PREFACE

Since April 20, 2020, Dr. James A. Tompkins has been addressing the critical topic of restarting the economy by telling public and private leaders the following:

- Governments, with the guidance of health experts, closed the economy by issuing stay-at-home orders. But governments, with the guidance of health experts, lifting their stay-at-home orders does not open the economy nor return business to “normal.” To reopen the economy:

- Business supply chains must restore the synchronization of supply and demand.

- Consumers must be willing to dismiss their personal stay-at-home orders.

- The economy must adapt to what will evolve over time as the “next normal.”

- The reality of the next normal as per the award-winning Japanese author Haruki Murakami:“And once the storm is over, you won’t remember how you made it through, how you managed to survive. You won’t even be sure whether the storm is really over.But one thing is certain: when you come out of the storm, you won’t be the same person who walked in. That’s what this storm is all about.”

- For the last three years, disruptions to business via digital innovations have occurred at an ever-increasing rapid rate. For the last two months, the black swan disruption to business from the coronavirus has resulted in the momentous slowing of the U.S. $22 trillion economy.

- The reality of business leadership today is best explained by the 1987 U.S. Army War College coined term VUCA. VUCA was created to help the government deal with the heightened levels of volatility, uncertainty, complexity and ambiguity resulting from the end of the Cold War.

- March and April 2020 have exhibited an unprecedented level of VUCA for the U.S. and global economy. Reopening the U.S. economy must be done business by business.

- The first step requires disciplined triage to determine which businesses should be saved, paused or closed.

- Once it is decided a company should be saved, VUCA 2.0 (Vision, Understanding, Courage and Adaptability) must be pursued.

- VUCA 2.0 will be different for each firm and must be deployed rapidly.

- Confusing the governments’ lifting of their stay-at-home orders with the reopening of the economy will result in further VUCA and damage to the U.S. economy. As Vice President Pence said on Sunday, April 19, “The Trump administration wants to be sure that the coronavirus cure isn’t worse than the disease.”

- We all need to focus our attention on restarting the economy to place the evil of COVID-19 in our rear-view mirror.

The purpose of this document is to present the details and thought processes that resulted in the above six-point preface. Each of the above six points is a section of this document as follows:

1.0: THE PROBLEM

The U.S. economy was booming in early 2020. As the Chinese population migrated back to their hometowns for the annual Lunar New Year celebration there were early reports of a virus that was very infectious and resulting in fatalities. As the virus spread, people were isolated in their hometowns and could not return to their places of work. The Chinese economy was brought to its knees and the virus began to spread to other countries. China is often referred to as “the factory of the world” as it produces a significant portion of the materials used by other countries in the manufacturing of products, as well as a significant portion of the finished goods. The Chinese manufacturers SUPPLY the materials for manufacturers around the world.

Figure 1: Supply Chain Mega Processes

The flow of materials and finished goods around the world is accomplished via the supply chain. The typical processes of the supply chain are illustrated in Figure 1 above. The materials were planned and bought from China but not made there because the Chinese factories were closed. Planning by the companies buying the materials was done by forecasting their demand and then buying the materials that allowed them to fill the forecasted demand. In fact, one of the key objectives of supply chain management is to synchronize the supply and demand of products as they flow around the world in order to minimize cost and drive a company’s profitable growth. The virus in China had a major impact on the supply of materials around the world and thus the demands could not be filled, resulting in product shortages. The reopening of the Chinese economy was very unpredictable as there was a ripple effect that required restarting. The ripple effect encountered the following set of “Problem/Go/Problem/Go” etc. as follows:

- The factory did not have workers

- Workers came back to work

- The factory did not have required materials

- Workers came back to the materials’ suppliers

- Truck drivers to deliver materials from manufacturers to the factories were not available

- Truck drivers came back to work

- The factories started manufacturing

- Truck drivers to deliver products from the factories to the port were not available

- Truck drivers to the port came back to work

- The ports did not have workers to unload trucks and load ships

- Port workers came back to work

- Ships sailed to their destinations with critical supplies of both materials and finished goods to provide the much-needed supply

The disruption of the ripple effect as a result of the Chinese virus was huge. Demand for products went unfilled. But then just as the supply to Western countries was restored, the Chinese virus also arrived. The virus did not arrive aboard the ships of products, but instead aboard airplanes carrying passengers with the virus. As the virus spread in the Western countries, stay-at-home orders were put in place that had a major impact on the demand for products. For discretionary products, demand disappeared and for health-related products, demand doubled, tripled, etc. For some products, the demand shifted. For example, overall use of toilet paper did not grow, but it shifted from the single-ply business toilet paper to the double-ply consumer toilet paper. Since folks were staying home, the demand for business-to-consumer toilet paper grew, but demand for the business-to-business toilet paper disappeared. In a similar way, think about tomato juice. Before the virus, there was a supply chain planning function that determined how much tomato juice to put into a 64-ounce, 46-ounce, 32-ounce, 28-ounce, 12-ounce and a 5.5-ounce bottle. Before COVID-19, the highest-selling juice for food service (restaurants) was the 64-ounce size and the best-selling juice among grocery stores was the 12-ounce size. Now, however, in the days of stay-at-home, the best seller is the six-pack of 12-ounce bottles of tomato juice and sales of the 64-ounce size have been close to zero. The interesting question is what will happen to tomato juice consumption one week, four weeks, eight weeks, etc. after the stay-at-home order is withdrawn. The point is the reopening of the economy certainly requires the lifting of the stay-at-home order, but once the governments decide to lift the order, what will be the supply chain process to synchronize the supply and demand?

A second factor impacting the reopening of the economy has to do with the consumers’ willingness to return to the “old normal.” As time evolves after the lifting of the stay-at-home order, how will people react to sitting in a restaurant 18 inches away from another customer eating dinner? How will we respond to working out in a public gym, getting a massage, having our nails done, sitting at a crowded sporting event, concert, play or bar, or boarding an airplane or a cruise ship? How will e-commerce grow moving forward? The consumer will for sure remember COVID-19; the question is, how will COVID-19 impact their lives and habits going forward and how does the reopened economy respond to the next normal?

Certainly, the quote from the award-winning Japanese author Haruki Murakami must be taken into consideration here:

“And once the storm is over, you won’t remember how you made it through, how you managed to survive. You won’t even be sure whether the storm is really over.

But one thing is certain: when you come out of the storm, you won’t be the same person who walked in. That’s what this storm is all about.”

2.0: INNOVATIVE AND CRISIS DISRUPTIONS

We are living today in an unprecedented time in the evolution of the world, the global economy and the supply chain that supports the global economy. This unprecedented time is the result of an unprecedented level of innovative disruption and crisis disruption. These two types of disruptions are peaking at the same time. If only an innovative disruption or a crisis disruption were peaking, the supply chains of the world would be shattered, but now in the spring of 2020, both types of disruptions are peaking. It is interesting that I have worked in supply chain for over 40 years (even though the term ‘supply chain’ was not used for the first 20 years) and my wife has always struggled to explain to anyone what her husband does. Finally, I find legitimacy because every night on the evening news, the term ‘supply chain’ is used over and over. I no longer have an illegitimate profession. Hallelujah, I am relevant! The next two subsections cover these two types of disruptions and why they are creating an unprecedented time for managing supply chains.

2.1: INNOVATIVE DISRUPTION

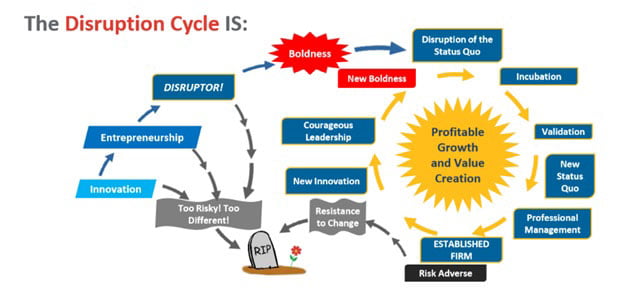

The level of volatility we are experiencing today is driven by the rise of digitalization and the frequency of change, also known as the “disruption cycle.” The disruption cycle (shown in Figure 2) is turning nonstop, beginning with an innovation, which sometimes leads to entrepreneurship or-if it’s too risky-winds up dead. Businesses that move on from entrepreneurship will become disruptors, but some of those will wind up dead too. However, those that harness innovation and boldness will disrupt the status quo. They then move through the incubation and validation phases before becoming the new status quo and, with the addition of professional management, they then become an established firm. It is at this phase where those that are too risk averse or resistant to change will end in death. Businesses that live through this stage and on to innovation, courageous leadership and new boldness will achieve profitable growth and value creation and become the new leader(s). Today’s digital era has produced the highest level of innovative disruption in all of history.

Two key observations about the disruption cycle:

- The speed of traveling around the disruption cycle is increasing. Thirty years ago, an organization traveled around the cycle once a decade. Fifteen years ago, a loop around the cycle took five years, whereas today, the cycle is traversed once a year or faster.

- Each company has two choices with the disruption cycle-disrupt the industry (proactive) or be disrupted (reactive). When a company is both the established firm and the disruptor, they will surge past the competition, gain market share and achieve profitable growth.

Figure 2: The Disruption Cycle

2.2: CRISIS DISRUPTION

Crisis disruptions can result from a wide variety of events. Below is a list of the top 15 crisis disruptions of 2018, in order of frequency of occurrence. The top 15 accounted for 90% of all crisis disruptions of 2018.

- Mergers and acquisitions

- Factory fire or explosion

- Reorganization

- Business sale or spinoff

- Factory slowdown or disruption

- Regulatory change or tariffs

- Extreme weather

- Hurricane, typhoon or cyclone

- Earthquake

- Labor strike

- EMA, FDA or OSHA action

- Fine or recall

- Power outage or shortage

- Labor action or settlement

- Port disruption

Interestingly, in the top 30-which account for 99.8% of all 2018 crisis disruptions-the topic of human health or pandemic is not mentioned. Additionally, at the end of 2019, a panel of global trade experts presented the top 10 crisis disruptions they predicted would occur and nothing related to human health or pandemic was mentioned.

Another way to look at crisis disruptions is by the impact they have. Impact can be measured on the local, regional or global level and can also be viewed by severity. A special category of crisis events that have a huge global impact are referred to as black swan events. Black swan events are events that:

- Have never happened before or are extremely rare (highly improbable events)

- Take people by surprise as they never imagined such an event occurring

- Carry a massive transformational impact

- After its first occurrence, the event is rationalized in hindsight, as if it could have been expected (even if it could not)

Clearly, COVID-19 is a black swan event.

The frequency of black swan events has been increasing, as is evidenced by these events:

- 1990: Recession

- 2001: 9/11 terrorist attack

- 2008: Mortgage crisis

- 2014: Ebola

- 2019: COVID-19

Each of these black swan events has had major impacts on the economy and what was considered normal. In fact, all black swan events result in the creation of the next normal.

3.0: VUCA

The concept of VUCA-Volatility, Uncertainty, Complexity and Ambiguity-was first introduced by the U.S. Army War College in 1987 to describe the state of the world following the Cold War. The term can also be applied to the business environment, where the VUCA of today’s increasingly digital world is having a tremendous impact on supply chains and commerce.

3.1: WHAT IS VUCA

Volatility

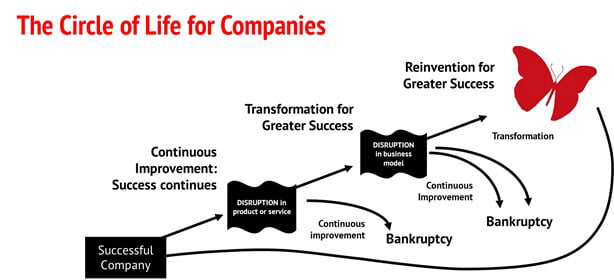

Volatility is all about change-the nature of change and frequency of change. The nature of change is best illustrated by bugs. Take, for example, the ant: when a baby ant grows into an adult, it gets bigger, but there is no change, which is represented as continuous improvement. Then there are grasshoppers, which experience transformation through changes in wings and reproductive organs. Lastly, the caterpillar undergoes total metamorphosis-or reinvention-as it becomes a butterfly. The circle of life for companies requires completion of all three steps-continuous improvement, transformation and reinvention-in order to be successful in today’s digital world.

Figure 3: The Circle of Life for Companies

In addition to the nature of change, we also have to look at the frequency of change, also known as the “disruption cycle.” As described in Section 2.1, the pursuit of the disruption cycle is innovation and boldness that disrupt the status quo. Those that successfully navigate all the way through the disruption cycle and on to new innovation, courageous leadership and new boldness will achieve profitable growth and value creation, and then the cycle repeats.

Uncertainty

We are living in the most uncertain times in the history of the world. The high level of uncertainty today makes it impossible for us to make accurate predictions or define standard operating requirements. Instead of developing optimal solutions, we need to focus on developing flexible supply chain solutions that are capable of adapting and constantly evolving to offer a series of options. When Popeyes failed to accurately predict the popularity of its chicken sandwich, the fast food chain blew through its entire inventory of the new menu item more than a month earlier than projected.

Optionality is the new optimality. Since you cannot predict what the future holds, make sure you have the greatest number of options available so when uncertainty hits, you can move to the option that will meet the requirements of that day-or moment.

Complexity

The rise of digitalization and increased complexity of commerce today is requiring companies to “sell anywhere” and embrace a unified performance. While there used to be a clear distinction between retailers, distributors, manufacturers and wholesalers, those lines are now blurred, from grocery stores developing their own private label brands to consumer packaged goods (CPG) companies creating their own e-commerce sites and selling direct-to-consumer (D2C).

To achieve success, companies must “fish where the fish are” by selling anywhere their customers are. This includes diversifying your sales strategy to incorporate all the channels and methods used by each of your customer demographics. When developing a strategy, companies must think beyond traditional digital and physical channels and evaluate all options, including mobile, desktop, social media, retail e-commerce, marketplaces, brick-and-mortar and more.

When broadening your sals strategy, it is important to maintain a single, unified supply chain, which is where complexity comes into play. This complexity drives the need to unify our channels, logistics, marketing and technology to act like a single company-or supply chain-and provide customers with a seamless shopping experience.

Ambiguity

As we enter a new era of business, there is a haziness of reality, or inability to understand what is really going to happen, that is taking place across all companies and industries. Digital technology is affecting all businesses by paving the way for new products, services and business models. In this digital era, it is imperative for all organizations to vigorously pursue digital commerce and prevail among the lack of certainty today. The COVID-19 pandemic is also fueling a rise in ambiguity, as businesses and consumers alike are unsure about what the next normal will look like.

In addition to the digital imperative, we are also battling the speed imperative. The speed at which the marketplace is changing its mind is much faster than the speed at which companies are able to respond. With the speed imperative, it is not about how fast you work today, it is about the rate of acceleration. If it is taking your organization weeks to make a decision that should only take days, your company will fall behind and become a victim of the speed imperative. Likewise, the half-life of a great idea is much shorter than it used to be due to the speed of disruption. As the pace of life is accelerating, you need to act faster than ever before.

3.2: HOW TO RESPOND TO VUCA

With today’s unprecedented level of VUCA, it is impossible to predict what the future holds. COVID-19 has revealed the weaknesses in traditional supply chain models, with the introduction of the virus in China in January and the ripple effect it created in supply chains and commerce that-like the virus itself-continued to spread across the world in the subsequent months.

The rise of digitalization and frequency of innovative and crisis disruptions require organizations to rethink their supply chain strategies and focus on building “anti-brittle” solutions. Instead of seeking ways to optimize their supply chains, organizations need to “optionize” their supply chains, deploying flexible and agile solutions that are capable of adapting and evolving to provide a series of options to address whatever is happening at any given moment. Anti-brittle supply chains operate as a living system, enabling organizations to quickly and efficiently reconfigure strategies, structures and solutions as needed to achieve success, profitability and growth in times of VUCA.

3.3: VUCA AND COVID-19

The recent COVID-19 pandemic has catapulted us into the greatest state of VUCA, creating beyond belief impacts on life as we know it and causing major disruptions across the entire supply chain. From a record number of unemployment claims to a sharp decrease in GDP and significant performance issues due to increased demand, this is the most dynamic, uncertain time we have ever witnessed.

Government restrictions-including a stay-at-home order and the closing of all non-essential businesses-have further amplified the already volatile situation by significantly straining commerce and the global economy. The path forward requires more than just simply lifting these restraints-the supply chain infrastructure needs to be in place for companies to be able to restart operations. While the outcomes will vary and not all businesses will prevail, the innovation disruptions of the digital era coupled with the crisis disruptions from the COVID-19 pandemic require total reinvention and an intolerance for mediocrity to survive in today’s VUCA world.

COVID-19 will forever remain in our minds, just as the Great Depression did for the people who lived through it. How we respond to these difficult times will impact the rest of our lives. The key to success is playing the hand you were dealt like it was the hand that you wanted.

4.0: BUSINESS STATUS, VUCA 2.0 AND STRATEGY

Business status may be viewed from a macro economy perspective or from an individual company perspective. This document is 100% focused on the individual company perspective. Two excellent papers on the macro economy perspective from the Boston Consulting Group are included at the end of this paper in the Additional Resources section. In particular, the discussion in these two papers about “Flatten, Fight and Future” provide excellent context for addressing the individual company perspective.

There are two high-level status factors that guide the development of an organization’s strategy going forward:

- Prior performance

- Industry sector

The rating on prior performance is based on the strength or weakness of the business on the following factors (If you have the below, you are strong; if you do not, you are weak):

- Financial stability: Strong P&L statement, balance sheet, valuation, brand equity, cash flow, liquidity, credit availability, net profit margin, etc.

- Customer-centric: Great customer satisfaction, high repeat business, strong pipeline of new customers and leadership understanding customers’ expectations.

- Planning: Robust and well understood organization plan, strategic plan, contingency plan, marketing plan, customer acquisition plan, budget plan and succession plan.

- Execution: Clear priorities and accountability, strong metrics and feedback, responsiveness, discipline, maintain deadlines, methodical and decisiveness.

- Unique value proposition: Pervasive across the company, a focus on applying core competencies to making customers delighted and ambassadors.

- Energy: Passion for company success, high energy and engagement, collaborative, inspiring, aggressive, optimistic, a sense of urgency and an attitude of “getting it done.”

- Innovation: A spirit of openness and eagerness to get better every day, to improve, to slay all sacred cows and to have a digital path forward.

- Leadership: A high level of integrity and honesty, candid open communications, perseverance, optimism, adaptability and a good judge of people.

- Teamwork: A keen awareness of the tremendous value and importance of true partnerships with customers, suppliers and staff. Not one or two of these three, but all three.

- Culture: A progressive culture based upon organizational alignment, respect, profitable growth, intolerance for mediocrity, embracing diversity and having fun.

The industry sector has to do with how your industry fared throughout the COVID-19 disruptions. Some industries were HAVEs in that their industry did well and had ample opportunity to prosper. To the contrary, the HAVE NOTs saw a reduction in business and few opportunities to enhance success. From a high level, here are the HAVEs and HAVE NOTs coming out of COVID-19:

| HAVEs | HAVE NOTs |

|---|---|

| Drug stores | Airlines, airports & TSA screening |

| E-commerce & delivery | Cruise lines |

| Janitorial services | Engineering & consulting services |

| Grocery stores | Events, conventions & trade shows |

| Pharmaceutical products | Fitness centers, spas, hair & nail salons |

| Security services | Food, beverages, restaurants & schools |

| Streaming services: Netflix, Hulu, etc. | Hospitality, tourism & Airbnb |

| Walmart, Target & Costco | In-store retail, malls & luxury goods |

| Wine & spirits | Sporting goods |

Given our prior performance ratings of weak and strong businesses and being in a HAVE or HAVE NOT industry sector, we can see one of four paths for each business:

- If you entered COVID-19 as a weak business and you are in a HAVE sector, you must pursue Doom to Boom.

- If you entered COVID-19 as a strong business and you are in a HAVE sector, you must pursue Boom to Boom.

- If you entered COVID-19 as a strong business and you are in a HAVE NOT sector, you must pursue Boom to Hibernate.

- If you entered COVID-19 as a weak business and you are in a HAVE NOT sector, you must pursue Doom to Tomb.

To grasp the overall strategy to follow the paths of Doom to Boom, Boom to Boom, Boom to Hibernate and Doom to Tomb, it is best to understand the work done by Bill George, a senior fellow at Harvard Business School who argues that VUCA calls for a leadership response which he aptly refers to as VUCA 2.0:

- V, instead of Volatility = Vision

- U, instead of Uncertainty = Understanding

- C, instead of Complexity = Courage

- A, instead of Ambiguity = Adaptability

Applying the VUCA 2.0 philosophy to the four business paths results in the following strategies:

The strategy going forward for a Doom to Boom business is very similar to the strategy for a Boom to Boom business. The only difference is in Doom to Boom greater care must be exhibited to preserve cash and to not spend ahead of new revenue. The Doom to Boom and Boom to Boom steps to follow are:

- Refine/revise vision to seize new opportunities and communicate to all staff.

- Check in with all key customers, retain revenue and aggressively pursue new revenue.

- Hire additional marketing and sales talent and redo messaging to make it consistent with the new vision.

- Protect key staff and suppliers.

- Confirm financial plan and stability are in place and adequate liquidity is available.

- Ensure accountability, the right team, high quality and customer delight.

- Reorganize as needed and ensure compensation/incentives are consistent with the path to success.

- Accelerate and remove all barriers to speed. Be agile and responsive.

- Develop ramp up plan for business and supply chains.

- GO! GO! GO!

The steps to follow for the path of Doom to Hibernate are:

- Maintain good customer relationships, ensure quality and productivity.

- Maintain revenue and look for opportunities to grow revenue with current clients.

- Reduce costs to a minimum to maintain service.

- Ensure financial stability and liquidity.

- Develop a hibernation plan and timeline to come out of hibernation.

- Communicate the hibernation plan to employees and ensure alignment.

- Maintain brand, reputation and optimism.

- Stay alert to happenings to come out of hibernation, be agile and flexible.

- Refine plan for exit from hibernation.

- Exit hibernation.

Lastly, and most painful, due to the closing of the business, below are the steps to follow the path of Doom to Tomb:

- Meet with co-owners or Board and agree on dissolution.

- Retain attorney and accountants to support dissolution.

- Develop dissolution plan and timetable.

- Share dissolution plan and timetable with employees and customers.

- Cancel financial commitments, collect AR, pay AP and outstanding debt and sell assets.

- Close out with bank, state, IRS and local agencies.

- Distribute remaining cash and assets.

5.0: THE IMPACTS OF THE SUPPLY CHAIN ON THE ECONOMY

5.1: A Brief History

In 1975, I:

- Was given an honorary discharge from the U.S. Army

- Began a full-time position as an Assistant Professor of Industrial Engineering at North Carolina State University (NCSU)

- Started a consulting business called Tompkins Associates

My area of expertise at NCSU was facilities planning, material handling and industrial logistics. My consulting focus was distribution (warehousing, network design, inventory and transportation). The distribution consulting business was not well respected and only a few leading firms (AMOCO, Miller Brewing, Kraft, General Mills, IBM, Berkline, Hayworth, Herman Miller, R.J. Reynolds, Ford and American Motors) would engage distribution consultants. By 1985, however, firms began to grasp the significance of distribution consulting and Tompkins Associates grew:

- To not only do consulting but also implementation of our solutions to include technology and material handling integration

- Globally

- To become Tompkins International

The profession of distribution consulting and implementation became respected and then evolved into being called “supply chain.”

The term supply chain was first used in the early 1900s, but early uses of the term were not talking about the processes of Plan-Buy-Make-Move-Distribute-Sell (Figure 1) or a system performing the processes of Plan-Buy-Make-Move-Distribute-Sell, but rather about the “Move” process. Then in the 1980s, consultants began using the term supply chain to describe a firm’s internal processes of Plan-Buy-Make-Move-Distribute-Sell. These internal uses of the term were not really about the supply chain, but more about a “supply link.” This discussion beget considerable bantering about not only supply chain, but also the terms “supply and demand chain,” “value chain,” “efficient consumer response,” “quick response,” etc. until the year 2000 when I wrote the definitive book, “No Boundaries,” which was then revised in 2003. The first six words I wrote in the introduction of the 2003 edition were “This is not your parents’ economy.” The point I was making with these six words is that the supply chain had huge implications on the economy of the world. The supply chain was not about the activities of a company (their internal supply chain), but more about a company and that company’s:

- Suppliers: Their suppliers, their suppliers’ suppliers, etc.

- Customers: Their customers, their customers’ customers, etc.

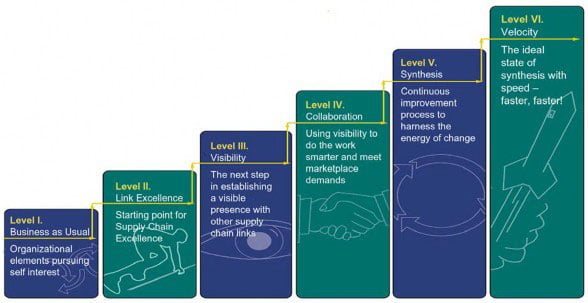

Another way to be clear about the scope of the supply chain not just being the internal supply chain (supply link) and more about the companies and all their suppliers and customers is to use the term end-to-end (E2E) supply chain. In the 2003 edition of “No Boundaries,” I used Figure 4 to illustrate and explain the evolution from:

- Focus on individual departments within a company (Level 1)

- To the internal supply chain (Level 2)

- To an informed internal supply chain (Level 3)

- To a first attempt of an E2E supply chain (level 4)

- To a significantly improve E2E supply chain (Level 5)

- To an evolutionary process of E2E supply chain excellence (Level 6)

Figure 4: Six Levels of Supply Chain Excellence

Level 1: Business as Usual. At this level, a company works hard to maximize its individual functions. Organizational effectiveness is not the focus. Instead, each organizational element attempts to function well on its own. Each division/department applies its own strategy for applications used.

Level 2: Link Excellence. This link eliminates and blurs any boundaries between departments and facilities and begins a never-ending journey of continuous improvement. Its individual link must evolve to make it the most efficient, effective, responsive and holistic that it can possibly be.

Level 3: Visibility. Links work better when they share information. Visibility establishes the groundwork for information sharing. It minimizes supply chain surprises because it provides the information links need to understand ongoing supply chain processes.

Level 4: Collaboration. Collaboration is achieved through the proper application of technology and true partnerships. Through collaboration, the supply chain can determine how best to meet the demands of the marketplace. The supply chain works as a whole to maximize customer satisfaction while minimizing inventory.

Level 5: Synthesis. Synthesis is a continuous improvement process that integrates and unifies a supply chain. Synthesis harnesses the energy of change to address a turbulent marketplace and ensure customer satisfaction. It is from synthesis that true Supply Chain Excellence is achieved because it enables a supply chain to reach unparalleled levels of performance.

Level 6: Velocity. The goal becomes accelerating the organization or supply chain to a higher velocity. Velocity creates shorter time frames, and this begets demand-driven.

Clearly by 2012-when digital commerce began to take hold-the profession of supply chain was highly respected, and companies began creating Chief Supply Chain Officers (CSCOs). By 2015, the role of the CSCO was well known and the role of supply chain was given a seat at many Board level tables. The profession of distribution had evolved from the backroom to become the end-to-end (E2E) supply chain and landing in the boardroom.

Then in 2019, we witnessed the E2E supply chain stream for digital commerce merging with the E2E customer journey stream to form and evolve into a new E2E river.

5.2: Digital Commerce Today

One of the major shifts in digital commerce is the introduction and fueling of the ways in which supply chains are “pulled” vs. “pushed.” Traditional chains were used to “push” products downstream to maximize their availability-at retail or other points of sale. Competition for shelf space has been the primary driving factor; however, most companies have found ways to complement that with advertising, promotions and other merchandising actions that create or stimulate demand, thus enabling the push.

Some companies have adopted strategies that lean more on “pull.” If customers demand enough, then supply chains can justify providing enough, without incurring large storage costs. This strategy has proved quite profitable for those companies that were able to “sell one, make one, ship one” as an operations strategy. Lean inventories translated into less working capital and less carrying costs.

The digital commerce revolution put this thought on steroids. Customers today decide what to order, when to order and how to order. Let’s consider what we have termed the customer journey.

We have identified the following 11 steps for an end-to-end customer order:

- Need/Want

- Discover

- Research

- Assess

- Select

- Purchase

- Receive

- Use/Consume

- Maintain

- Influence

- Repeat

While not every customer goes through all 11 steps for each order, most do, whether deliberate or not. These are not business processes-they are customer actions (or thoughts) that are commonly involved in the journey. They also are not sequential or simultaneous. Customers may delay, spend more time researching or dive deeper into any of the steps. The important point is that there is a series of steps that customers undergo for an online order, and many sellers work to affect these via advertising, increased visibility and other customer-centric actions.

We can also categorize these steps as follows:

Steps 1-4: SHOP

Steps 4-7: BUY

Steps 7-11: USE

Thus, the three mega-processes for the customer journey supply chain are SHOP, BUY and USE.

5.3: The Merger of the Two E2E Streams (Supply Chain and Customer) Becomes the New “E2E River”

Digital commerce managers have not understood that the two streams do indeed merge. The customer works through their mega-processes until they decide to BUY. The SHOP processes depend on where they go to find, consider and evaluate the products that fill their needs, wants or “must haves.”

The BUY, of course, triggers the traditional supply chain to work. And, the USE depends on the supply chain for “after-sales support,” influencing other BUYs and returns.

So what does this mean to corporate supply chains? The answer is much more than commonly thought. First, the two streams are interconnected. Second, they influence each other, especially when they merge into the new “E2E river.” Third, they interact at multiple points in the processes.

It is this new E2E river that must be addressed for digital commerce efficiency and effectiveness. It is more meaningful than simply providing customer personalization, which is necessary but not sufficient.

Let’s next consider how the new E2E river is different from the two separate streams.

- Identification. Before successful reinvention can occur, companies must recognize not only the need but also the appropriate approach for implementing a customer-centric supply chain model. Merging the corporate supply chain with the customer journey requires a thorough understanding of how these two historically separate processes work together to deliver a single, E2E supply chain solution. With consumer demands constantly changing and growing, today’s supply chains need to be flexible and capable of delivering a series of options to address the needs of that moment.

- Interconnectivity. In order to operate as one cohesive solution, it is important to understand how the new customer shopping journey and the corporate supply chain model influence each other as well as sub-processes. One area of particular importance is inventory management. Striking the balance between supply and demand in today’s retail landscape is more challenging than ever, as customer demands for rapid, free delivery continue to grow and storage space is expensive and limited. To accommodate customers and also cut costs, many companies are now adopting a “pull” or demand-driven strategy, where products enter the supply chain after a customer places an order, resulting in leaner inventories and lower carrying costs. Employing a sophisticated inventory optimization tool, along with a powerful distributed logistics network, is essential to creating a seamless customer experience.

- Visibility. While contributing to the death of nearly 10,000 retail store closures in 2019, the proliferation of digital commerce has also created new channels and opportunities for companies to attract customers. Since different audiences shop at different places, it is important to diversify your sales strategy to incorporate all the channels and methods your target customer groups use to shop for goods. In addition to new sales channels, companies must maximize visibility across various stages of the shopping journey. Social media offers a wealth of opportunities, from enabling sellers to connect directly with customers to providing a venue for conversations with friends and family, which also heavily influences customer purchases.

- Integration. Implementing an E2E supply chain solution requires a robust technology stack capable of adapting to changing customer and market demands and managing multiple channels and strategies. Utilizing a comprehensive digital platform that connects, integrates and automates a company’s entire sales and supply ecosystem enables a true E2E supply chain and an amazing customer experience.

The global and domestic economies are driven or destroyed by the new E2E river, also known as the E2E Digital Commerce Supply Chain. The E2E Digital Commerce Supply Chain creates many opportunities for revenue growth, operational cost reductions and enhanced customer satisfaction.

At the same time, failure to embrace the E2E Digital Commerce Supply Chain will result in failure of the supply chain to synchronize supply to demand while also incurring increased operating costs and poor customer satisfaction. Clearly, supply chains have a major impact on the economy, especially in times like today where innovative disruption, crisis disruption and VUCA reign.

6.0: A PATH FORWARD

The discussion has evolved:

- From WHO should open the economy?

- To WHEN to open the economy?

- To HOW to open the economy?

On April 24, the answers for the U.S. seem to be:

- The governors should open the economy for their states while following federal guidelines

- The economy should be open when it is clear COVID-19 is in significant decline

- The economy should be reopened:

- In phases, while meticulously studying the trends and being prepared to judiciously change direction

- While fully retaining social distancing

- While protecting workers by providing them with face masks and hand sanitizer and implementing temperature monitoring

At the same time, there are some limited discussions of understanding the next normal, but weak leadership on how to:

- Resynchronize supply and demand

- Alter product offerings

- Understand how to deal with consumer health concerns

- Understand VUCA and how to respond to VUCA

- Address a global recession

- Communicate a company vision and path forward

- Address the E2E Digital Commerce Supply Chain challenges

To reopen the economy (See the Appendix for a full explanation of the Reinvention Success Playbook and Process):

- The government must, in a timely fashion, lift the stay-at-home orders.

- Company leadership must understand the role of supply chain in reopening their company.

- Company leadership must get their organization aligned around a detailed strategy and path forward for reopening their company.

- Company leadership must successfully pursue their strategy and path forward for reopening their company.

When key companies and industries are open and addressing the next normal, then-and only then-will the economy be reopened.

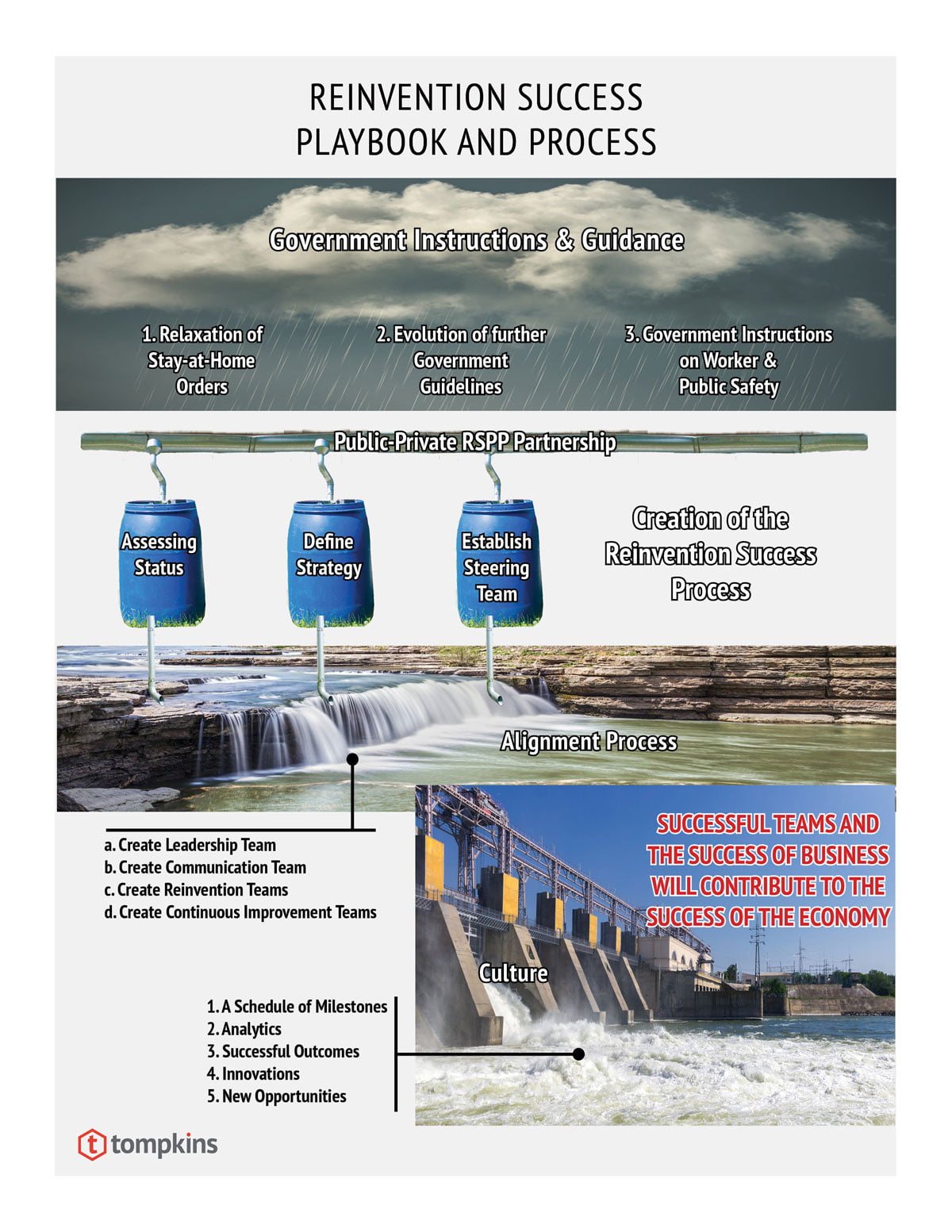

APPENDIX: REINVENTION SUCCESS PLAYBOOK AND PROCESS

Each business must develop their own Reinvention Success Playbook and Process (RSPP) to guide their path to success on the other side of COVID-19. This RSPP is not about reopening the business or recovery for the business, but rather the reinvention of the business. Recall in Section 3.1 where we likened reinvention to the metamorphosis of the caterpillar into a butterfly. Yes, many businesses will crawl out of the stay-at-home orders on their stomachs, but they will fly out of their RSPP as beautiful butterflies: reinvented by success. Figure 5 illustrates the seven-step process a business must pursue to undergo their success metamorphosis, from crawling on their stomach through the COVID-19 shutdown to entering their cocoon of the RSPP and coming out as a reinvented butterfly and successful business contributing to the recovery of our previously booming economy.

The RSPP is presented metaphorically in Figure 5. The Government Instructions & Guidance is a cloud that rains down the three valuable guiding edicts:

- Relaxation of stay-at-home orders

- Evolution of further government guidelines

- Government instructions on worker and public safety

This rain is caught by the public-private RSPP partnership gutter and directed into the three rain barrels of:

- Assessing status

- Define strategy

- Establish a Steering Team

As the water flows through the rain barrels into the turbulent white water, the Reinvention Success Process is created by:

- Creating the Leadership Team

- Creating the Communications Team

- Creating Reinvention Teams

- Creating Continuous improvement Teams

The creation of this process calms the white water and the powerful, aligned river flows downstream for the waiting hydropower dam that converts the energy of the flowing water into the power of electricity. The hydropower plant represents the culture of the company being reinvented and the flow of water through the hydropower dam represents the five outputs through the dam of:

- A schedule of milestones

- Analytics

- Successful outcomes

- Innovations

- New opportunities

The metaphor is complete when the energy generated by the RSPP produces successful teams and a successful business that will contribute to the reestablishment of a successful economy.

Figure 5: The Reinvention Process

Step 1 of the reinvention process entails the federal and state governments and the health experts making critical decisions about the health and safety of everyone living in or traveling to America. This step must involve:

- Deciding when and how to relax stay-at-home, business, school and events orders.

- Monitoring health analytics and being prepared to judiciously issue new or evolving orders or guidelines.

- Issuing and evolving social distancing, public safety, worker safety and other guidelines deemed appropriate as needed.

Step 2 of the reinvention process is building upon the Public-Private Partnerships (PPPs) that have evolved in Washington, D.C. as an effective tool to address major issues, where the partnership between the government and industry has the ability and power to bring about change more than if either party operated alone. PPPs have been used to create public awareness of COVID-19 and work on testing, vaccines and therapies. What is needed now is a PPP that focuses on a COVID-19 RSPP to return America to the economic prosperity it was experiencing in the beginning of 2020.

Step 3 of the reinvention process consists of three parts:

- Assess Status: As presented in Section 4.0, there are two high-level factors that guide the development of an organization’s strategy:

- Prior performance: either “Weak” or “Strong”

- Industry sector: either “Have” or “Have Not”

This assessment must be done by the firm’s C-level executives and must be done quickly. At this point in the process, the organization must assess the 10 factors presented in Section 4.0 and should not do a deep dive. The goal is to conduct a high-level assessment of the business to feed into the development of the organization’s overall strategy.

- Define Strategy: Based on the status assessment, a decision must be made if the path forward for the company is to close the business, hibernate or build the business to new levels of excellence and success. It may be decided that some divisions of the business should be closed, some should hibernate and some should begin now building a new future. These decisions should be scrutinized by people with an intimate understanding of the business as a mistake at this level could significantly hurt an organization’s ability to reach their best destination. Outside industry experts should be consulted if there are conflicts among the C-level to ensure this step is done well.

- Establish a Steering Team: After conducting the status assessment and developing the strategy, a Steering Team must be created. In most organizations, the Steering Team already exists and-for the most part-already functions as a team. The Steering Team should have 5-10 members and consist of the top executive and their key staff. The Steering Team has the following two tasks:

- Steering the organization: The job of the Steering Team is to refine the strategy from Step 2, establish the vision and serve as the initial communicator of the strategy and vision. Steering Team members should individually and collectively demonstrate a focus on the strategy and vision and must consistently and persistently work toward the vision alignment.

- Steering the RSPP process: Through the definition, guidance and motivation of the Leadership Team (established in Step 4), the Steering Team should guide the overall RSPP process.

Even though the Steering Team members may also be part of the Senior Executive Team, Executive Team, Management Committee, Policy Committee, etc. and have a regular meeting time and modus operandi, this team should be called the RSPP Steering Team and have a regularly scheduled meeting solely for Steering Team business.

Step 4 of the reinvention process includes the creation of the following four teams:

- Leadership Team: The Leadership Team provides the leadership and operates as the workhorse of the RSPP process. To do this, the Leadership Team must work toward vision alignment by defining, chartering, orienting, encouraging, motivating and accepting accountability for the Communications, Reinvention and Continuous Improvement Teams. The Leadership Team should consist of 8-16 well-respected people involved in all aspects of the company. The leader of the Leadership Team should be a well-organized, action-based person who understands the company’s supply chains and possesses strong communication skills. The Leadership Team should meet weekly and proactively help each team overcome obstacles and difficulties. The Leadership Team should follow this process:

- Orientation

- Define priorities

- Charter teams

- Provide team orientation

- ‘Encourage, motivate and support teams

- Ensure team progress

- Monitor and report results

- Grow process

- Return to Step 3: Charter Teams

- Communications Team: Most organizations have two things in common:

- Poor communications

- Leadership that cannot understand why poor communications exist

Leadership is troubled, as they have worked hard establishing and then using a formal communications system. This formal communications system is top-down. Typically, bottom-up and horizontal communications do not work. The fact is, information and the understanding of information is power-they are to an organization’s RSPP process what gasoline is to an automobile. This is even more critical during times of reinvention and COVID-19 recovery because if people do not have the information, the informal communications system will generate information that will most likely be detrimental to the process. Or going back to the analogy, when the automobile lacks gas, people in the midst of chaos put water in the gas tank. For an organization to be successful at RSPP, a top-to-bottom, bottom-to-top and side-to-side communications network must be established and used. Additionally, customers and suppliers, along with all staff, need to have clarity on the strategy, vision and path forward. It is the responsibility of the Communications Team to ensure that these communications take place and that everyone in the organization has a clear understanding of the strategy and the vision, the status of teams and the organizational status. The Communications Team often consists of 10-20 members and meets on a regular weekly basis.

- Reinvention Teams: The Reinvention Teams are responsible for the application of the disruption cycle (Figure 2) to reinvent a business or supply chain. They are charged with using innovation, entrepreneurship and disruption to develop new ways of reducing costs, increasing revenue, improving quality and/or increasing customer satisfaction. Reinvention Teams use blue-sky, out-of-the-box, breakthrough thinking and creativity to achieve significant improvements in performance. Multiple Reinvention Teams can exist in a location, unlike Steering, Leadership and Communications Teams, where only one team of each type exists for a company location.

- Continuous Improvement Teams: While Reinvention Teams are interested in step function improvements as a result of creativity, Continuous Improvement Teams are focused on a continuous flow of small incremental improvements. Continuous Improvement Teams achieve results by unleashing the power of the people. In most organizations, there are literally thousands of ideas in the minds of workers that would significantly improve operations. These ideas will be surfaced, vetted and implemented via Continuous Improvement Teams.

Step 5 of the reinvention process is all about achieving organizational alignment. Indications that organizations are properly aligned are:

- Every person in a company shares an understanding of the strategy, vision and status of the organization.

- Every person in the company knows how they contribute to the company’s success.

Alignment is the behavioral and emotional interconnectedness of employees to the organization’s strategy and vision. In these VUCA times, it is clear more than ever that establishing and increasing organizational alignment is a fundamental necessity and should be a primary target of businesses today to ensure reinvention success. A key success factor of alignment is when individuals at an organization accept the responsibility for making the organization’s strategy and vision a reality. Some important guidelines in achieving alignment are:

- Organizations do not get aligned-people do

- People only become aligned when there is a compelling, practical benefit to it

- Alignment is a process that must be nurtured over time

- Alignment requires a personal decision of enrollment

- Alignment is to an organization what a magnifying glass is to sunlight-it provides a powerful focus and allows things to really heat up

Step 6 of the reinvention process will produce great outcomes if the first five steps are done well and the culture is right. Culture is a foundation upon which organizations are built. It permeates every organizational activity and event and allows one to interpret all that occurs. Each organization has a unique culture that plays an important role in its success. Existing cultures work to maintain the existing culture, but in times of innovative and crisis disruptions, there is a tremendous opportunity to develop a dynamic culture. In the wake of COVID-19, our cultures are being shaken and questioned. It is critical in these VUCA times that we retain our culture of optimism, high integrity and determination. It is very important that we adopt a culture of being proactive, accountable and having a sense of urgency. What will then flow from the first five steps and our enhanced culture are the fruits of our labor:

- A schedule of milestones

- Analytics of important performance criteria

- Progress and successful outcomes

- Innovations and breakthrough performance

- New opportunities not previously seen or understood

Step 7 of the reinvention process is the energy that flows from the process. This energy will power the organization to the next boom and more. This boom will result from successful teams and will enable the reopening and success of the company and contribute to the success of the economy.

COVID-19 Resources

Tompkins International

Navigating the VUCA of Today’s Digital Commerce World

Jim Tompkins

Anti-Brittle: Succeeding and Flourishing in these Uncertain and Volatile Times

Jim Tompkins

COVID-19: Win the Fight, Win the Future

Boston Consulting Group

Beyond the Curve: How to Restart in the Wake of COVID-19

Boston Consulting Group

CONTACT INFORMATION:

Jim Tompkins

Founder and Chairman

Tompkins International

6870 Perry Creek Road

Raleigh NC 27616

(D) 919.855.5501

(M) 919.637.2508

Email: jtompkins@tompkinsinc.com

Assistant: Debbie Flynn, 919.855.5447

ABOUT THE AUTHOR

James A. Tompkins, Ph.D.

Founder and Chairman, Tompkins International

Dr. James A. Tompkins is an international authority on designing and implementing end-to-end supply chains. As the founder and chairman of Tompkins International, his focus over the last several years has been in the areas of digital commerce, unichannel and supply chain reinvention, helping companies connect supply chain processes with the customer journey to increase long-term profitable growth. Jim coined the phrase ‘Sell Anywhere,’ which is the strategy of selling through a wide range of online and offline channels where consumers shop, buy and enjoy products, offering a seamless, end-to-end customer experience.

Jim received the prestigious Frank and Lillian Gilbreth Industrial Engineering Award from the Institute of Industrial Engineers (IIE) on June 1, 2015. The award is an attribute that recognizes Dr. Tompkins through the contributions he has provided to the welfare of mankind in the field of industrial engineering. In addition, Jim has served as President of the IIE, the Materials Management Society and the College-Industry Council on Material Handling Education and has been named a Distinguished Engineering Alum by Purdue University. He has also received more than 50 additional awards for his service to his profession.

Over the last 40 years, Tompkins International has evolved from a supply chain consulting firm into an end-to-end supply chain consulting and solutions company, with business units focusing on supply chain consulting services, material handling integration, applied technologies and robotics, which together form a true end-to-end digital commerce ecosystem. His 40-plus years at Tompkins International and his focus on helping companies achieve profitable growth give him an insider’s view into what makes great companies even better. As a high-level business and supply chain strategy advisor, his unique perspective prepares corporations and executives for the future.

Jim is a thought leader, sharing insights on business strategy through his presentations and videos, including his most recent, Anti-Brittle: Succeeding and Flourishing in these Uncertain and Volatile Times. Jim also shares his knowledge and provides up-to-date information on supply chain and business trends via Linkedin and Twitter.

He has written or contributed to more than 30 books, been quoted in hundreds of business and industry magazines such as The Journal of Commerce, Supply & Demand Chain Executive, DC Velocity and FORTUNE, and has spoken at thousands of international engagements.

Jim received his Bachelor of Science in Industrial Engineering in 1969, his Master of Science in Industrial Engineering in 1970 and his Ph.D. in 1972, all from Purdue University.