Adapting to the ‘China Factor’

Gene Tyndall

EVP, Global Supply Chain Solutions

Tompkins International

September 2011

www.tompkinsinc.com

* Note: For the purposes of this paper, the term “Asia” as used here does not refer to Japan or Korea, as these countries have moved beyond emerging markets. The focus is mainly on Southeast Asia, with a strong emphasis on China.

Introduction

As supply chain management becomes a more dominant force in executive suites, questions arise about its contributions to profitable growth – not just for bottom-line operational excellence, but also for top-line revenue improvement.

Positive examples of the effects on shareholder value are being seen in almost all industry sectors, as the supply chain leaders outperform their competitors.

While many organizations are just beginning to learn about the supply chain’s value potential, others do not yet recognize it. Thus, this position paper was developed to explain how the supply chain impacts shareholder value and to provide guidelines on how any company can leverage its processes to increase or create that value.

The rapid and expansive growth in China – and throughout Asia – continues to amaze, excite, and challenge business leaders around the world. Its huge market potential for profitable growth, however, is only beginning to be understood.

This paper on the “China Factor” deals with the enormous impact of China’s growth on the whole of Southeast Asia, as well as on the rest of the world. Taking into account the principles of a value creation framework – profitable growth, margin improvement, and capital efficiency – this paper discusses how global supply chain actions and value drivers impact these three major categories of value.

Addressing Asia opportunities and the “China Factor” is vital for global supply chains today, and this paper demonstrates how to leverage shareholder value while expanding into these new and challenging markets.

1.0 The Supply Chain Value Creation Framework

The importance of supply chains and their effectiveness, or lack thereof, has never been more apparent. As the global economy continues to show some signs of recovery, albeit slow, and consumers resume buying, supply chains are back at work.

But this time, more than ever, the scope is global and the strategic importance is crucial.

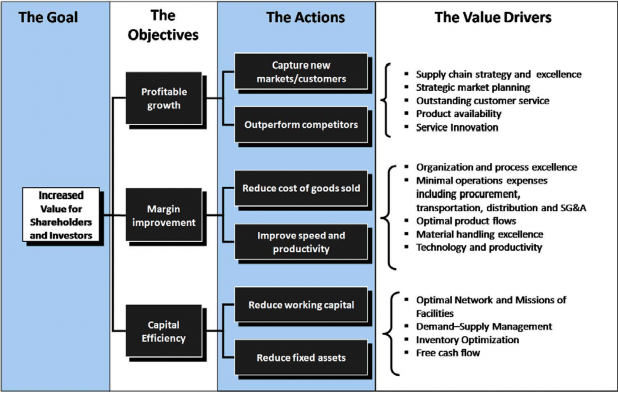

Figure 1: The Supply Chain Value Creation Framework

Figure 1 depicts why supply chains are important: They drive value, which ultimately reaches shareholders and investors. With profitable growth, margin improvement and capital efficiency all being impacted, it is clear why today’s CEOs and boards are paying more attention – actions taken with supply chains create value for any company that buys, makes, or sells a product or service.

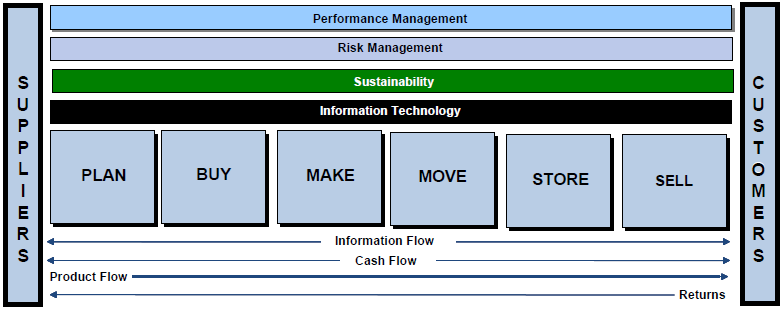

Moreover, new understandings have surfaced of what supply chains are really all about today. The supply chain mega processes, PLAN – BUY- MAKE – MOVE -STORE – SELL, shown in Figure 2, comprise the operations of the business. The four flows – Materials/Products, Information, Cash, and Work Flow – determine the effectiveness and efficiency of the operations.

Most companies have traditionally managed these mega processes as functional silos, with little information shared across functional boundaries. In today’s global economy, a supply chain is likely to have many interrelated trading partners spanning geographies, time zones, and cultures.

Figure 2: Supply Chain Mega Processes

Using the “The Supply Chain Value Framework” within an organization is an excellent way to engage team members toward a common and indisputable goal: shareholder value. As companies examine opportunities for profitable growth, margin improvement, and capital efficiency, this framework helps keep process leaders focused on the end game. It ensures that within each mega process key value drivers are identified and prioritized. Benchmarking and adapting best practices is another important method to help ensure that the right actions are initiated and sustained.

“Value creation” is at the core of the Supply Chain Value Framework and, thus, within the mega processes. If we believe that the most important value creator is “cash” (and most studies bear this out) then we can look to supply chains to create cash, minimize its uses, and speed up its flows.

2.0 Profitable Growth

All growth is not profitable. As the Value Framework in Figure 1 depicts, capturing new markets/customers or outperforming competitors are certainly growth drivers. However, pure revenue expansion for the sake of growth may be the absolute wrong goal.

2.1 Capture New Markets/Customers

Growth strategies are a means to counter stagnation, enhance performance, and increase revenue. The key to finding the right growth strategy is properly matching it to the company and its specific marketplace. Typically, several combinations of strategies are used within a company’s strategic objectives. Figure 3 shows high-risk and low-risk strategies.) Potential profitability should be examined before any type of growth strategy is deployed.

Figure 3: Southeast Asia Market Entry Strategies

The first step in developing a proper growth strategy is to examine all types: diversification, market development, product development and market penetration. The supply chain becomes a key focus in all aspects of growth. Two vital questions for each strategy are: (1) Can the existing supply chains be leveraged, and (2) can they handle the additional capacity the growth strategy promises to deliver? The same high-to-low-risk market entry analysis shown in Figure 3 applies to the Asia and China markets just as they do to any around the world.

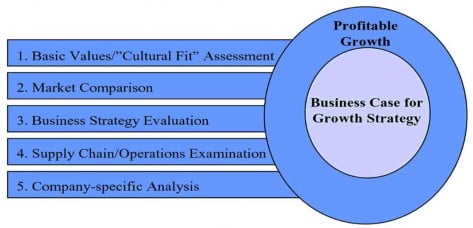

There are five relevant filters that can be used to focus your growth strategies (below, and see Figure 4):

-

Basic Values Filter: As many different areas as possible are tested for their “cultural fit” with the company. This can lead to an early exclusion of certain products or markets.

-

Market Filter: Potential opportunities are put to a market test by defining them in terms of size, market maturity, market cyclical dependencies, competitiveness and profitability.

-

Strategic Filter: The existing business model in the target areas must then be measured against the company’s own strategy. A good choice of appropriate selection criteria helps the company not only define new areas of business but also more clearly define strategic guidelines of the existing business. Possible criteria include the degree of value creation (trade versus production versus services), similarity to existing key competences, the required human resources, and the breadth of the customer profile.

-

Supply Chain Filter: The supply chain filter allows a company to decide if it wants to use its distribution operations or if it needs to invest in new operations – or increase efficiency of current operations. A company will need to evaluate how the processes and procedures may change with the additional products or revenue.

-

Company-specific Filter: In the event of a merger or acquisition, potential companies must be identified for integration. The criteria for the acquisition – target revenue, target profitability, target geographic focus, and culture, among others – must be established to determine the best fit.

Figure 4. Five Filters for Creating a Growth Strategy Business Case

Growth strategies are an important part of a company’s overall business strategy, and the Asia markets are no exception. Careful planning and due diligence will assure that the growth strategy will be successful and contribute to the company’s overall revenue and profitability. The most important planning involves evaluating the type of growth strategies to be considered and then applying a filter. The business plan will identify the addressable market, value proposition, competitive advantage, key factors for success, and entry options to further define the opportunity. Regardless of the type of growth strategy deployed, the supply chain will be a key focus for operational efficiencies.

2.2 Outperform Competitors

Top-performing companies often maintain a dual focus: meeting and exceeding profitable growth objectives and outperforming competitors. In order to achieve these goals, it is critical to have a strategic market plan and the supply chain capabilities in place to deliver superior results (surpassing the competition). It is also vital that this strategic market plan addresses both internal and external activities. Within this section of the paper, three key areas (market focus, communication and responsiveness) that enable companies to outperform competitors are examined.

Focus on the Market

The prime attribute of most top-performing companies is the most basic of business strategies: a focus on the market. Top-performing companies regularly develop and revisit a Strategic Market Plan (SMP) to ensure that they understand customers’ needs and wants better than their competitors. In support of an SMP, organizations need to continuously gather information about customers and markets, but this is just the starting point.

Additionally, companies should understand what is happening within the global environment (including the ‘China Factor’). It is important to gather and track information on government regulations and policies (local, national, and international), industry technological advances, current and future industry trends, and last but not least, what direct competitors are doing.

There is no substitute for having experts within Asia who understand the cultural, political, and business climate, as well as what your top competitors are doing.

Communication

Sources for this information include trade publications, industry conferences and events, corporate and individual networks, and internal and external research reports. A mountain of information is available, and there are numerous ways to attain it. Yet, the real value can only be unleashed if it is packaged and delivered in a meaningful manner throughout the company. This leads to the second key requirement in enabling companies to outperform their competitors: communication.

Companies that go through all the work of understanding customers, markets, operating environments, and competitors must also ensure that they have a way to communicate this information throughout the organization. There are various means of communication ranging from informal and low-cost alternatives – such as newsletters, e-mail blasts, and management Q&A forums – to more formal technology-driven solutions, such as market databases and CRM applications. But the mode of communication is not nearly as important as consistently sharing business intelligence that employees can use to strategically respond to the market. Many of today’s global supply chain information technology applications support both the collection, as well as the dissemination, of this critical data in a timely manner.

In addition to being able to convey customer and market information to employees, strong internal communication also directly affects profitable growth through higher employee retention rates and getting more input from employees in ways that will improve the business. Furthermore, companies that outperform their competitors are the ones that coach and mentor managers to communicate effectively with employees, follow a formal communication process, and connect employees to their business strategies.

Respond to What Has Been Learned

Lastly, top-performing organizations not only collect the best information and communicate it throughout the company, they also respond to what has been learned. Generating and communicating the information is one thing, but unless there are changes based on what is learned, nothing has truly been accomplished.

This step is the hardest one to implement because it crosses so many functions within a company. Having an integrated and responsive Sales, Inventory and Operations Process (S&OP), combined with more timely and accurate information than competitors, as well as a proven, consistent means to communicate that information throughout the company, is what enables top companies to consistently outperform competitors. Responses to changes in customer needs, wants, or market conditions may include updates to current products, new product introductions, entering new global markets, new distribution channels being opened, outsourcing of non-core activities, and shifting of inventory or components from one region to another, to name a few.

2.3 The Asia Opportunity – Exciting And Challenging

Everyone understands that China has become the “world factory” in an unprecedented short timeframe. In less than 20 years, China has risen to a world power in producing goods in almost all industry sectors. Now it is time to consider new opportunities – sales and distribution for China’s rapidly expanding middle-class consumer markets.

The New China Opportunity

Since China joined the World Trade Organization in 2001, exports have expanded 25% each year. Even with some diversification of the supply base to other Asian countries over the past few years (especially Vietnam, Indonesia, and Bangladesh) and some concern about rising costs (labor, land, environmental, and utilities), the “China Factory” continues to expand and is expected to soon become the largest manufacturing country in the world.

The factor that is often overlooked, however, is the unprecedented growth of consumers in China. Estimates of the population levels with discretionary income are now over 100 million, and this is growing at over 15% per year.

In addition, business-to-business sales are increasing as new companies start up to serve various markets. Almost every industry segment within China is experiencing rapid growth in consumer, commercial, and industrial markets.

The government has announced its intent to diversify the country’s manufacturing base and population centers in the west. Currently, over 90% of the growing “middle class” and trained workers are domiciled in the east and southwest of China. This includes the first-tier metropolitan areas of Shanghai, Beijing, and Shenzhen. Thus, the government is targeting new city centers and is committed to building the infrastructure to enable this rapid growth to occur.

In less than a decade, China will have a national highway system to cover all its cities (old and new), its logistics parks, all container ports, and 300 airports. In addition, railways and “short-sea” transport for inland rivers are planned.

The expansive new transportation system, combined with incentives to locate factories and services throughout the country, will serve more than just the rural population. This strategy will also enable the migration of trained workers west (to some, to go “back home”).

These expanding consumer and commercial markets will occur more rapidly than any other time in history, as China commits multi-billions of dollars to its development.

Income levels of individuals in China are expected to rise at least until the government is satisfied that there is a large enough domestic consumption market to balance imports and exports. Along with that consumer expansion will come commercial development that will be limited only by economic factors. Business opportunities, therefore, are becoming enormous in China.

Sales and Distribution Challenges with the China Factor

The question many business executives are asking is, “How do we best take advantage of this new opportunity?” As North American and European companies that are sourcing for finished products in China recognize the expanding domestic markets, some are beginning to sell selected products into selected channels.

Moreover, as other multi-nationals look to the expanding markets, they are beginning to sell by importing finished (or near-finished) goods into China for sale.

There are multiple challenges, however, in selling and distributing products to customers within China. Some of the main challenges are outlined below, along with the key questions that need to be resolved for each company’s unique situation:

-

Strategies

-

Who are our customers, and how do we sell to them?

-

Who are our competitors now, and who will they be in the future?

-

How should we market our products?

-

-

Complexities

-

How do we get started?

-

Do we need a Chinese partner company?

-

How do we find the right partner(s)?

-

-

Risks

-

Aren’t there risks involved, such as intellectual property loss and counterfeiting?

-

How do we identify and mitigate the risks that will affect our investment?

-

How will we know how to price our product lines?

-

-

Variability in Demand

-

How can we forecast sales?

-

What can we do to manage the demand swings of fickle customers and buyers?

-

How will we do market research within China?

-

-

Evolving Distribution Infrastructure

-

How will we know where to locate distribution facilities?

-

How will we be able to track improvements in logistics and transportation?

-

What will our costs be for storage, distribution, and order fulfillment?

-

-

Product Quality and Supplier Effectiveness

-

If we assemble and package final products in China, how will we control quality?

-

How do we handle returned goods?

-

What are the labeling compliance rules?

-

-

Import/Export Issues

-

How can we maintain compliance with customs laws and regulations?

-

How do we classify commodities properly?

-

How should we manage the costs of transportation and logistics?

-

-

Knowledge and Talent

-

Where can we find knowledgeable managers, sales staff, and other employees?

-

How will we maintain current knowledge on consumers and track buying behaviors and preferences?

-

How can we ensure that we are following best practices available in China?

-

Resolving Issues and Growing Profitably

Whether your company currently sources and buys products in China – or would like to export products to the China markets – it is imperative to first meet challenges head-on by addressing the right questions.

Organizations will need to rethink their sales and distribution strategies to incorporate China and Asia. End-to-end supply chain solutions are no longer just an option – they are a necessity in order to successfully tackle emerging markets. Applying a holistic approach to your global supply processes will yield the greatest return on investment.

Another essential strategy is to have experts on the ground in China who can guide you through strategy development and lead you through operations (processes, people, and technologies), start-up, and execution.

In fact, it is the strategic planning and execution of global supply chains that will enable profitable business growth throughout Asia as the region moves from an emerging to a booming market.

Companies that achieve profitable growth and outperform competitors use a Strategic Market Planning (SMP) process to deliver timelier, more robust, and better business intelligence than the competition. These same companies have proven means of using global supply chain technologies to share information throughout the organization to provide employees with business intelligence in a constant, clear, and succinct manner.

Lastly, the companies that have proven S&OP processes in place – enabling them to take what has been learned and respond accordingly – will outperform their competition in China and throughout Asia.

3.0 Margin Improvement

Operating margins represent the difference between operating revenues (sales) and operating costs (expenses). For a company that makes, buys, or sells product, it reflects the total costs of that product. It also reflects the productivity with regard to producing, buying, distributing, and servicing the product.

Thus, the company needs to work on reducing the cost of goods sold (COGS), as well as productivity and speed. In addition, supply chain decisions impact the taxes paid by the organization around the world, which also adds to the costs of operations.

3.1 Reduce Cost of Goods Sold

The total COGS comprises all the operational costs that go into its transformation from BUY through to SELL – in other words, the supply chain (Figure 5).

Figure 5. End-to-End Supply Chain Planning

BUY

Many people view buying (or procuring) as purchasing – a necessity of business – and, thus, discount its ability to positively impact margin. However, the BUY process has a distinct role in securing products and materials as a critical integrated component of the supply chain. It is this integration that makes the procurement a significant cost and value driver. Procurement has the potential to deliver the best price, the highest quality, and the best availability through the development of an agile supply base.

Procurement Process to Deliver Best Price

Clearly, favorable pricing lowers the cost of goods and contributes to improved margin. The best ways to do this, however, are not so clear. Aggregating volume is typically the first step to improved pricing. However, many companies lack visibility to what they are spending with each supplier. The procurement process should pursue spend analysis (gather all purchase order details and segment these purchases into commodities and groupings) to gain visibility and control over purchases. Selecting two or three suppliers to source particular goods will increase volume and gain additional leverage to negotiate better pricing through a larger quantity purchase per supplier.

Procurement Process to Deliver Best Quality

Poor quality often leads to rework, more labor, additional shipping, recalls and even money spent in reparations. In turn, these issues result in elevated cost and, therefore, should be minimized and avoided. Visibility into supplier quality can have significant impact.

Until a company pulls all operational components together between the supplier and customer (purchase order acknowledgement, on-time delivery, correct quantity, correct quality, and accurate invoicing) the true cost of the supplier-customer relationship be cannot be determined. Suppliers that ship the incorrect quantity, or invoices incorrectly, cost the company additional resources. Procurement can serve as the stewards of the supplier-customer relationship, monitoring all interactions and communicating back to the supplier. This level of relationship management can detect both administrative and product quality drifts, and proactively address them – minimizing impacts and additional costs.

Procurement Process to Deliver Best Availability

Customers would almost always prefer 100% availability from their suppliers. Yet as the service level requirement increases, so does the cost to the customer, as well as to the supplier. The supplier maintains the appropriate inventory to guarantee the desired service level; thus the price of the product/service is higher due to the embedded inventory carrying cost.

However, a knowledgeable procurement organization can help minimize demand variability by engaging with suppliers and sharing accurate forecasts, business strategy changes, production schedules, and product launches that significantly impact changes in demand.

Lowering demand variability helps a supplier plan for a more accurate demand, enabling improved service levels. This improved service level can have a significant effect on internal operations in which a more stable flow of goods/services can be planned for and executed more efficiently. Reduced demand variability equates to higher service levels and can translate into lower supplier inventory, which will result in lower pricing for goods and services.

Procurement Process to Deliver an Agile Supply Base

The ability of a company’s supply base to quickly respond to changes (e.g., change in demand, shifting of quality requirement, and changes in taxation) can help a company gain margin or minimize cost. Unfortunately, this agility is not an inherent trait of most supply chains and, thus, must be developed to a mature, effective state. Agility is especially important to global supply chains expanding into Asia.

A skilled procurement organization develops the business intelligence that alerts it to early failures, warns of changing demand and signals the magnitude of potential interruptions. It also performs risk analysis and develops secondary and tertiary supply alternatives. These proactive steps not only minimize time and resources lost during interruptions, they also reduce the cost associated with such events by preplanning and negotiating before the crisis to eliminate price gauging during high-demand, low-supply scenarios. Procurement manages information flow and supply chain risk that helps prevent margin erosion and minimizes impacts of supply chain interruptions.

Procurement should be the steward of a company’s supplier relationships and the broker of operational and supply chain information. Its unique position to interact with all supply chain processes allows it to obtain valuable insight into operational and supply details. This visibility can be leveraged to gain significant margin reduction through reduced pricing, improved quality, and maintained availability through variable demand.

By establishing the right strategy, designing efficient processes, staffing the right skills, enabling with the right technology and designing an effective organization, procurement can achieve an agile supply base that can deliver the best price, best quality, and best availability.

MAKE

The COGS for the typical manufacturing company ranges from 55% to 95% of total revenue and averages 80%. Even modest changes to the COGS can have a staggering impact on a company’s financial health. Making significant improvements in the COGS should be a high priority for all manufacturing companies. A 1% reduction can translate into a major improvement in gross profit margin.

The typical components of COGS in manufacturing are materials, labor, allocated overhead and tooling and equipment. The most effective way for companies to make improvements in these cost buckets is to either reduce wasted expenses in their manufacturing processes or have a core competency in outsourcing to world-class manufacturers for product supply.

Reducing waste in manufacturing requires an execution of lean tools to focus on the following waste categories through the MAKE process:

-

Overproduction: Producing more components and products than is needed by the next processing step creates waste in the form of excess inventory and increases the risk of damage and obsolescence.

-

Waiting Time: Whenever a person in the manufacturing process is waiting (non-value- added time), instead of adding value to the product or process through his or her job function, then time is wasted and cost is added. Elimination or reduction of waiting time is a fundamental concept in lean manufacturing.

-

Transport: The customer who is paying for a product is not willing to pay for movement (transport) of the products, components, or raw materials needed to produce a product. Reducing the need for movement of a product or reducing the distance moved minimizes the wasted time and cost for that movement.

-

Over-processing (unnecessary processing steps): Evaluate manufacturing processes to remove or reduce the time required for processing steps that do not add value to the product. An example would be applying two layers of coating to a product when only one is needed to create the quality of product required by the buyer of the product.

-

Excess Inventory: Inventory exists to buffer one step in a process from another so that no interruption will occur. If processes are synchronized to each other, the need for inventory is reduced and the investment in inventory can be minimized.

-

Unnecessary Motion: All motions that are performed by individuals to create a product must be analyzed to reduce all unnecessary motions. These superfluous motions create added labor in the process.

-

Defective Products: The production of defective parts and products wastes labor and requires quality control to ensure that defective product does not reach the customer.

In summary, reducing the waste in manufacturing processes through a focus reducing overproduction, waiting time, transport, over-processing, excess inventory, unnecessary motions and defective parts using the tools of lean manufacturing can be the best approach to reducing a company’s COGS.

MOVE

In recent times, the cost to transport raw materials, work in progress inventory, and finished goods to market has increased substantially as a percentage of COGS. While the economic downturn has eased rates and fuel prices in the short term, rates will certainly begin to rise again as shipping volumes increase.

Transportation decision makers are faced with many challenges, including customer requirements, mode selection, carrier/fleet capacities, shipment visibility, performance management and much more. The fact that transportation mode quality, routes and practices in China vary from region to region only complicates this challenge. Fortunately, transportation planners can apply best practices and technology to develop a well-controlled freight management program.

While there are a number of ways to reduce transportation operating costs, shippers can take advantage of some of the following options:

-

Develop Core Carrier Programs: Shippers that leverage their relationships well with their carriers typically experience lower rates and better service. Core carrier programs focus shipping volumes on approved carriers that meet an established set of requirements. Performance metrics are monitored and reviewed with those carriers periodically, and a collaborative relationship is developed to improve service and reduce costs.

-

Consider a Transportation Management System: Transportation management systems (TMSs) are available with a wide array of functionality and means of deployment. From routing software to full scope TMSs, there are applications available to meet every shipper’s requirements. TMSs are also available in the traditional self-hosted form as well as the Software as a Service (SaaS) approach in which the application is hosted by the vendor, enabling quicker and less expensive implementations for some shippers.

-

Gain Control of Inbound Freight: Many companies rely on their suppliers to manage the shipment of goods inbound for stock or direct to customers. Often, there is an opportunity to take control of inbound freight and improve service while reducing costs. The additional freight spend can lead to improved discounts and rebates for parcel and LTL for all shipments. Additional volumes may create opportunities to consolidate smaller shipments into lower cost freight modes. Of course, freight terms should only be transitioned where freight can be managed in-house more economically, and/or when suppliers can reduce COGS properly.

-

Consider Outsourcing Various Transportation Management Functions: Transportation Management Services Providers (TMSP) offer shippers the opportunity to outsource any or all transportation functions. Many shippers leverage TMSP services such as dedicated fleets, shipment planning and execution, brokerage, freight invoice auditing and payment, freight forwarding and more. Some shippers outsource their entire transportation management function. Shippers should explore which TMSP services may be advantageous.

-

Look for Shipment Planning and Execution Opportunities: Choosing the right shipping mode to meet service requirements is critical to controlling freight costs. Each mode has a sweet spot for freight characteristics such as weight, cube, etc.; however, at the margins of those ranges, there are grey areas as to which mode is more advantageous. For example, larger parcel shipments may qualify for hundredweight / multi-weight service or LTL. Larger LTL shipments may be less expensive via truckload service. Additionally, service levels should be carefully considered. For example, is next-day service required or can a package be shipped via ground? Examine opportunities to consolidate freight, such as creating multi-stop truckloads rather than shipping LTL. Pool distribution, deconsolidation, zone skipping, intermodal and many other strategies offer shippers a variety of solutions to consider.

-

Rationalize Fleets: Private and dedicated fleets offer guaranteed capacity and operational control. They also offer sound alternatives to common or contact carriage in scenarios such as short haul moves, highly sensitive customer deliveries, last mile, hazmat, specialized equipment and more. Evaluate fleets periodically to determine if their role, composition (assets and drivers), practices and technology meet requirements. Additionally, maintenance plans and fuel management are important to controlling costs.

-

Improve Controls: Establishing well-thought-out performance objectives and metrics is critical to successfully managing transportation performance, as it is with any other business process. Conduct periodic reviews internally, as well as with transportation management services providers and/or carriers. It is also important to apply cost controls when appropriate. Some examples include approval process for expedited shipments, carrier accessorial charge authorizations, and standardized accessorial fees and fuel surcharge programs.

In summary, taking control of freight spend through some of the steps outlined above can substantially reduce COGS and improve profits. Applying these strategies will not only reduce operating costs, but will also improve service and operational control.

STORE

There is an old saying in warehousing that goes, “If there is available space, someone will eventually fill it,” and this usually happens sooner than later. Therefore, it is not uncommon in most supply chains for warehouses and distribution centers to be full, even during slow periods.

Normally a storage facility will run out of space due to rapid growth, seasonal peaks, large discount buying, planned inventory builds for manufacturing shutdowns, facility consolidation, or even slow sales for the period. For consumer-driven environments in which seasonal planning and purchasing rely heavily on buying forecasts and shifting consumer tastes, the availability of the right merchandise to ship to the customer is vital to success and sales.

Hence, planners desire to have a wide selection of goods, as well as large quantities of “hot” items, to fill customer orders. When it comes to supply chain space planning, everyone is driven by demand and forecast accuracy.

However, when examining supply chains in general, warehousing is for the storage of materials that are used in manufacturing, packaging and assembly, while distribution centers are for the transformation of bulk products from a multiple-source shipment into a mixed load shipment.

Storage, unto itself, is rarely a key part of the supply chain formula for low-cost distribution, yet it can be a best practice to maximize sales, customer satisfaction, and reduce total delivered costs.

Although storage for cost reduction appears to be a contradiction, storage can add value, but it generally increases costs if it is not managed effectively or leveraged fully by planners, sales, and/or purchasing.

Distribution used for storage offers significant benefits for:

-

Managing long lead-time items including imports;

-

Buffering seasonal stock purchases to reduce risks;

-

Creating custom assortments to improve product sell through;

-

Converting bright stock into customer labeled stock, reducing over-production or future rework or obsolete stock;

-

Allowing for reserve stock to better manage shelf-level replenishment across multiple store or customers;

-

Increasing assortment mix and reducing fulfillment times by leveraging appropriate material handling and automation technologies; and

-

Buffering customer stock to reduce their risk, over-buys, and returns.

Best-in-class organizations achieve short- and long-term success by designing supply chain storage operations to support specific business requirements, to effectively leverage internal planning, purchasing or sourcing initiatives, and to reduce business risks to acceptable levels. This is never easy, as the space and labor to effectively manage inventory come at a premium. The application of best practices, operational-specific solutions, and process management strategies will reduce the total COGS and improve margins for all organizations in the supply chain. However, improperly designed and managed storage will simply be full all of the time or, worse, empty because it was not coordinated with improvements in inventory S&OP throughout the organization.

When looking at storage to reduce costs, here are 10 great ways to gain profitable growth through storage:

-

Strategic Positioning of Inventory – Drive sales with available inventory.

-

Product Protection – Keep product safe and undamaged, and secure add value.

-

Seasonal Buys – Buffer stock to reduce lead-time supply risks.

-

Special Deals – Take advantage of appropriate purchasing quantity opportunities and discounts.

-

Quality Assurance – Minimize recall risks with testing and aging holds.

-

Postponement – Use generic stock to fulfill customer-specific packaging and reduce production overruns.

-

Value-Added Services/Assortments – Create custom product mixes to increase sell through, labeling and tickets, as well as many other specialty services.

-

Returns Management – Improve customer experience and reclaim maximum inventory value (resell or supply chain control).

-

Freight Spend Reduction – Improve trailer and load utilization by staging and consolidating shipments within delivery windows.

-

Growth Management – Build inventory to meet rapid growth as well as leverage production and supply chain replenishment capabilities.

SELL

Companies often underestimate the contribution that operational excellence (i.e., supply chain) makes to growing their customer base. Operational excellence is key in: sustaining the position of the preferred supplier; creating and entering new markets; and taking market share from the competition. Effective supply chain management has as much to do with revenue growth as it does with margin improvement.

Management is learning that “pull” supply chains, stimulated solely by customer demand and characterized by customer service-intensive actions, do indeed contribute to revenue growth. Yet they also realize that, unless the company is 100% “make-to-order,” pull chains (also referred to as “demand-driven supply chains”) are complex to master and grow open-ended, unless the company is a catalog or Internet-based fulfillment business. Today’s marketplace of high fragmentation, more channels, and rapid product proliferation makes it even more challenging.

Differentiation through service value is the critical success factor. Amazon, for example, has raised the service bar to customer delight through easy ordering and speedy delivery of the right products. While many companies are beginning to measure the “Perfect Order,” the recognition that they are far from “perfect” becomes a wake-up call.

What is the “Perfect Order”? It is the order that is easy to enter, simple to track, delivered on- time as promised and in good condition, with perfect documentation, and accurate invoicing with easy payment. It also involves proactively notifying the customer of the order status, being responsive and keeping the order secure. Very few companies can report their “Perfect Order” rates as being in the 90% range.

“Perfect Order” is just one type of service that companies can use to differentiate themselves. Other services are made available by companies trying to achieve superior customer service. These organizations realize that differentiated customer service is not only profitable; it can be a true competitive advantage. An example of this is service bundling (i.e., channel-specific, product-service combinations developed to differentiate the company through service value).

Creating customer value is the end goal of the supply chain SELL process. By creatively improving the customer’s performance, value is created for both parties. In fact, most supply chain managers do not think strategically about this goal; rather, they measure (and are measured by) discrete benchmarks, such as on-time deliveries or order fill rates. The Procter & Gamble and Walmart partnership changed all of this by showing the world that an operations-based partnership could increase sales, reduce costs, and minimize working and fixed capital for both partner companies.

There are four key steps involved in planning and implementing profitable, differentiated service programs, and all can apply in Asia:

-

Segment Markets and Product Groups. Most companies do some form of market segmentation, and target marketing messages for discrete products to discrete groups. Yet, few companies develop segmentation strategies that help them ascertain where and how to create customer value.

-

Identify Key Value Points by Customer. All customers are not created equal. For each of the key customers, what elements of service would add the most value to their business? Cost reduction? Joint logistics? Collaborative planning? Joint promotions? Knowledge sharing?

-

Identify Consolidation Opportunities around the Customer. When evaluating their supply chains, companies often discover that separate chains exist for certain products, or from different product groups, that often flow to the same customer. This is often found in multi-divisional businesses that have organized themselves around product lines so finely that markets and customers have taken a back seat. Consolidating supply chains across products, across geographies, occasionally across channels, and even across customers and segments, can improve costs and services.

-

Identify and Create Common Processes and Systems around the Customer. Many companies have come to understand that the right balance of commonality can mean huge value payoffs in terms of the drivers of market value discussed here. Global, regional, and local supply chains that depend on the market, the product, the customer value proposition, and the common processes perform at higher levels. They also contribute to revenue growth.

There are various ways to satisfy ever-more demanding customers. The challenge is to find those methods that are profitable to both parties – those that create customer value as well as supplier value. Over-serving all customers (without corresponding value) is of course the wrong strategy, but likewise is the separation of sales and marketing from supply chain. The solution is to develop “service-products,” targeted to the right markets, segments, and customers, so that benefits will accrue to both parties. This is why SELL is a mega process of the supply chain.

3.2 Improve Speed and Productivity

The other major action to create value in margin improvement is through speed (doing things quicker) and productivity (doing things less costly and more efficiently). These are related, but not necessarily integrated. Yet, the full potential for margin improvement is to design business processes that are speedier and more efficient.

Speed

Do it quicker (and better). This is a common imperative these days. Speed to market for new products, tighter and more effective sourcing, more streamlined manufacturing processes, quicker movement through the DC, increased order picking efficiency, more frequent deliveries, and improved transportation transit times are all aspects of greater supply chain velocity.

However, there is an interesting juxtaposition to all this speed. Environmentalists and, in fact, economists suggest that sometimes slower is better. Ocean container ships are reducing steaming speeds (and thus fuel consumption) to something reminiscent of the days under sail. Low-cost country sourcing, while increasing the length and timeline of the supply chain, is financially attractive.

Nevertheless, the consumer’s desire for instant gratification and the ever-increasing risks of these extended supply chains are driving companies to rethink their sourcing policies. More and more, the economic focus is on “Total Delivered Cost” of goods rather than “Landed Cost.”

As such, the proximity of production to market has the environmental edge – all of which continues to feed the need for speed.

There is no question that the old adage of “the right product, to the right place, at the right time, in the right condition, for the right price” still rings true. “Time is everything” might be the mantra, but it must not be at the expense of customer satisfaction.

How do companies become quicker and smarter? They benchmark and leverage best practices. They develop strategic, tactical and operational supply chain action plans. They factor the supply chain into product development. They rationalize and strengthen supplier relationships. They employ the appropriate current technology. They optimize distribution network(s). They develop and monitor key performance metrics. They appropriately outsource where needed. They listen to the voice of the customer.

Perhaps the most important “how” is innovation. Being open to new ideas, designing modular and scalable operations/systems, and embracing connectivity through the Internet will generate the speed needed to remain competitive in the whitewater of change being experienced today.

The benefits of speed can be seen in areas such as:

-

Transportation mode optimization: improves delivery times, thus, increasing sales and reducing inventory in transit (lower inventory carrying costs);

-

Dynamic warehouse slotting: increases picking efficiency, and in turn, reduces labor costs; and

-

Pre-packed orders from suppliers: allows crossdocking at the distribution center, consequently, reducing handling, leading to reduced losses due to product damage and reduced labor in the receiving, picking and shipping functions.

As speed increases in these and many other areas, margins improve and shareholder value grows.

Productivity

Companies recognize that an improvement in productivity can have a direct improvement on the bottom line of their monthly budgets. So what are they doing to improve value and reduce the bottom line?

Within the supply chain, there are great opportunities to monitor and affect the current productivity with each element and across the entire supply chain. Productivity improvement can be found throughout the supply chain, but the two most frequent areas of focus are direct labor and materials.

Labor

Labor is the bread and butter of productivity. Enormous efforts have been used to create optimal lot sizes and improve changeover times in manufacturing to increase productivity because that is where a large focus on labor has been concentrated. The key is to understand which areas of the organization have not been challenged with improving productivity and combined with the greatest concentrations of labor to yield a prioritization. Where do companies have the most labor?

-

Is it in the manufacturing plant?

-

Is it in the call center, order fulfillment and/or customer service?

-

Is it in the transportation fleet?

-

Is it in the office and support operations?

-

Is it in the distribution center?

Knowing the number of full-time employees and cost is critical in assessing which areas will be prioritized.

Material

In addition, improving the productivity within material can be critical to the success of an organization. From raw material purchase to consumer sell, it is the one component that consistently moves within the entire supply chain.

Optimally, purchasing the correct quantity of material with the cost of handling calculated at different break points yields bottom line results throughout the entire process. Some effects include increased receiving, less space, lower utilities, reduced transportation, cost of capital for obsolesce, reduced replenishment labor and improved inventory turns.

As current technologies have continued to evolve within the supply chain, a continuous improvement process must be in place to evaluate internal metrics measure productivity levels and establish improvement goals. Some metrics include COGS per piece, COGS or handling per case, costs per transaction, turns, inventory accuracy, inventory, fuel consumption per mile, and more.

Metrics must be posted in a central, easily visibly and visual management system. Posting current activities and future goals on a frequent basis shows the entire workforce the importance of these factors in upper management’s dedication to improving the operation.

As the process to improve evolves, companies need to investigate complex scenarios for continuous improvement. Some considerations include:

-

Evaluating various automated material handling methods to handle products in consolidation centers;

-

Automating crossdock facilities that only hold minimal inventory;

-

Semi-automating loose-pick crossdock processes for promotions and weekly circulars; and

-

Examining other processes to yield higher productivity.

Every improvement in productivity is a bottom line, trackable metric that can be published and presented. These unbiased improvements provide increased value to the shareholder and investors.

3.3 Tax-Effective Supply Chain Management (TESCM)

One of the key factors contributing to shareholder value is the worldwide “Effective Tax Rate” (ETR) for companies that have operations on a global scale. The ETR is the indicator of all the taxes the corporation pays – based on the countries within which it operates, the size of the operations, the tax rates of those countries, and of course, the import/export duties and taxes for its goods movement.

The Asia opportunity presents the TESCM supply chain and tax planning processes with new opportunities for reducing taxes while still meeting operational requirements. Taxes vary by country, and sometimes even within a country – by province, for example. Moreover, the routing of goods through certain ports will vary the taxations.

The ETR is published in annual reports and in other publically available sources. The typical range for multinational corporations (MNCs) is 20-35%, with the average being about 25%. This is comprised of numerous tax rates – income, property, VAT, duties, sales, federal/state/local, assets (both tangible and intangible), and several more. Global tax experts have identified more than 20 different taxes that are paid by MNCs.

The importance of the ETR to a company’s financial health cannot be overstated. It is evident in its profitability, generation of free cash flow, and other measures of financial performance. It can seriously affect the company’s competitiveness, its ability to invest in growth, and its total delivered cost and product pricing.

Integrate Supply Chain and ETR

When a company undertakes a supply chain transformation, it can expect a 5-10% improvement in operating margins. If the ETR is not considered simultaneously, however, that operating gain could be neutralized by a higher ETR.

The fact that operating savings are viewed as “pre-tax,” avoids the true effect – that only 60% or so of these cost reductions will flow to the bottom line. Similarly, a 5% tax rate restructuring without concurrent supply chain optimization could increase the costs of operations at least that same amount.

Unfortunately, all too often these two business issues are not optimized together. Supply chain managers do not understand the ETR, and tax managers do not fully understand the rationale underlying the decisions on sourcing, facility locations, and the transporting and distribution of goods across borders to target markets. One important example of this disconnect is when supply chain managers seek to optimize the global network, locate facilities in which the flow of goods reduces the costs of transport/logistics, and then discover that the tax rates and/or incentives overrule the entire plan. Many companies make location decisions based on the #1 factor of tax, not supply chain costs.

Tax-Effective Supply Chain Management (TESCM) is the process of integrating tax planning into the overall management of the company’s supply chain. This process, of course, can be complex, dynamic, and conflicting, as tax laws and regulations change.

The allocations and locations of functions, assets, and risks, and decisions on transfer pricing, are inherent to the ETR, as well as to the optimized global supply chain. Even when a company has completed a TESCM analysis and an effective structure is in place, events can change the situation quickly – an M&A integration, for example, can obviate the entire structure, just as tax authorities can with changing laws and regulations.

Global Supply Chains

There are numerous methods available to tax planners and financial leaders to manage global cash, work with transfer pricing methods, obtain advanced pricing agreements (APAs), and manage financial risks. It is unnecessary and impractical for supply chain managers to understand these methods or apply them. However, it is important for supply chain, tax, and finance managers to collaborate whenever changes are contemplated in the global network of facilities, in the flow of goods, in the operations organization, and in the allocations or locations of assets.

The global supply chains of MNCs are particularly affected by the ETR, which is growing more visible to senior executives and boards. Yet, surveys show that less than 50% of MNCs have truly tax-effective supply chains, and even fewer have a formal process for safeguarding their tax or operating benefits.

Any company, however, that sources, transports, and/or distributes goods across borders will be assessed taxes that can put it at the higher rate category, thereby limiting its profitability and its competitiveness.

The achievement of Tax-Effective Supply Chains may appear too complex or challenging for many. Yet the benefits – lower costs of operations and ultimately, true profitability and free cash flow rates – are too important to ignore. Working collaboratively, operations and finance managers can make a significant difference in their company’s shareholder value.

4.0 Capital Efficiency

The capital efficiency of a company is measured by how well it manages its assets, both fixed and working. Fixed assets are those that are owned – plants, equipment, real estate, vehicles, computers, etc.

Working capital is required to finance the business. Although it is usually tied to inventory, it also involves other capital needs.

4.1 Reduce Working Capital

Working capital to finance inventories is determined completely by the supply chain strategy. The mega processes of the supply chain define how, when, where and how much is bought, created, deployed, stored and serviced.

Inventory

Capital efficiency can be maximized through effective inventory management, specifically by minimizing inventory working capital while ensuring the required level of customer service. Inventory working capital has two primary components: (1) cycle stock, which cycles regularly through replenishment and consumption cycles; and (2) safety stock, a customer service hedge against forecast error, lead-time variability and related issues.

Cycle stock is an economic issue. That is, how often do companies need to acquire additional product and what quantities are required? The economics are minimized by balancing the period acquisition transaction costs with the inventory opportunity, risk and storage holding costs for each SKU-stocking location.

Cycle stock is minimized by:

-

Stocking only inventory that cannot be economically acquired (manufactured or purchased) after the demand has been received and, then, only in location(s) that are either economically justifiable to minimize transportation expenses or to maintain demand order cycle time requirements;

-

Acquiring inventory (that must be stocked) in dynamically determined, economically optimum order quantities;

-

Using an S&OP process as a management framework for effectively addressing and resolving conflicting demand/supply issues; and

-

Operating an ongoing program of reverse logistics to reposition overstock.

Safety stock is a business philosophy issue – what level of product availability is to be provided? In some cases, the optimum level of customer service can be determined based on economics. In many cases, however, it is a judgment to be made by management across the complete product line.

Safety stock is minimized by:

-

Determining the optimum level of customer service for each portion of the product line;

-

Determining safety stock quantities based on the desired customer service level on an ongoing, dynamic basis;

-

Reducing acquisition lead times and lead-time variability and increasing the completeness of receipts through an effective Supplier Relationship Management (SRM) program;

-

Maintaining accurate information on on-hand balances.

Above and beyond the specific actions noted, both cycle and safety stock can be minimized by:

-

Accurate forecasting of routine demand and one-time demand events;

-

An effective business process for new SKU creation, forecasting and determination of initial acquisition quantity;

-

An ongoing program of SKU rationalization, supported by an effective SKU discontinuation business process;

-

Measuring, reporting, reviewing and continually improving inventory performance; results in both financial and customer service areas.

Cash-to-Cash Cycle Management

In virtually every industry, there is evidence of a never-ending quest to further improve business, while increasing efficiency, as well as drive greater profits to the bottom line and more cash to the bank. While there are many tools and approaches for continuous improvement, finding a comprehensive yet simple approach to measuring the impact of both operational and financial gains from such improvements remains a key focus for successful organizations. Furthermore, world-class companies are striving for metrics to benchmark themselves against competitors and industry standards in order to further identify and leverage improvement opportunities to their strategic advantage.

Perhaps one of the most widely available and used measurements is the focus on improving the cash-to-cash (C2C) cycle. This cycle is generally defined as “the length of time a company’s cash is tied up in working capital before it is returned in the form of collections of receivables.” In other words, this spans from the point of investing capital in inventories and labor to produce goods (and services) that are then delivered (sold) and, ultimately, paid for by customers.

Similar to any other asset, cash is useful when it is “available,” and conversely, is not useful when it is not available. For example, a machine that is idle in a factory is “waste,” and inventory that sits idle over time unsold in a warehouse is also “waste.” Cash is also “waste” when it is not in the company’s bank account and not available to create new value.

In reality, for many businesses, the period of time that cash is “unavailable” while in the cash-to- cash cycle is simply unavoidable, given the normal commercial terms most companies use in the normal course of buying and selling. However, if this cycle time is measured (in days), and tracked over time, compared to competitors and industry averages, a company can use this information to identify and drive improvements by targeting and actually lowering its cash-to- cash cycle days over time.

Calculating C2C

So how is the cash-to-cash cycle calculated? For product-based companies, it is the number of average days that cash is tied up in inventory and receivables, less average days’ use of Accounts Payable (A/P) dollars (for COGS). The calculation, which is a derivation of inventory, Accounts Receivable (A/R) and A/P “turns,” is simply converted to “time” as measured in days, as follows:

Add: Inventory C2C (days cash tied up in inventories) = Avg Inv / COGS x 365 days

Add: Receivables C2C (days cash tied up in uncollected AR) = Avg AR / Net Sales x 365 days

Less: Payables C2C (days use of cash before paying for inv) = Avg AP / COGS x 365 days

When the resulting calculation is positive, this indicates that cash is being “tied up” for more days in unsold inventory – raw materials, work in progress (WIP), or finished goods – and uncollected receivables, than the number of average days gained from use of vendor/supplier’s cash.

If the result is a negative number, however, cash is being effectively leveraged to produce a “net availability” of cash from operations – which, of course, is quite desirable.

While many companies may not consistently achieve negative “days,” it is the effort to identify and implement ways to reduce the cash-to-cash cycle time that keeps the organization focused on continuous improvement to drive the metric to (or below) zero. For example, if average inventory is $1 million with COGS of $8 million, then the inventory C2C equals 45 days ($1M/$8M x 365 days).

Similarly, if average A/R is $2 million and net sales is $16M, then the receivables C2C equals 45 days ($2M/$16M x 365 days).

Combined, cash is clearly tied up in working capital for 90 days before the organization considers how effectively A/P is leveraged. To complete the calculation, if average A/P is $1.3 million with the same COGS of $8 million, payables C2C equals 61 days, resulting in a total C2C of 29 days (90 day – 61 days).

For service-based industries, a fourth metric may be used, similar to payables C2C, whereby the amount of cash tied up in average payroll cycle is measured, and deducted from inventory and A/R C2C days, as follows:

Less: Payroll C2C (days use of cash before paying payroll) = Avg P/R accrual / COGS x 365 days

From a practical standpoint, ensure that industry-comparable C2C standards also include this fourth factor as well. This can be quite meaningful for companies in which inventory is either minimal or non-existent, as a means of benchmarking how well it deploys cash for its (human) resources.

Benchmarking C2C

The C2C cycle number on its own, for a single year, has little value unless compared to competitor or industry norms. Because this is a widely used measure, obtaining benchmarking cash-to-cash data is relatively easy, and thus, enables a company to compare itself to others, for the purpose of identifying which of the three areas to improve.

Such comparisons form the basis of strategic planning, and should be followed up by defining specific actions to improve the cash-to-cash cycle. This could be part of an already-existing continuous improvement program or lean manufacturing model.

For example, if this same company, in comparing total C2C of 29 days to an industry average of 13 days, finds that the inventory C2C industry average is 30 days (versus the company’s 45 days) – while it compared well on A/R and A/P industry averages of 45 days and 61 days – the area to improve cycle time obviously lies in inventory reduction.

The company may then identify actions to improve inventory flow, decrease turns, reduce or eliminate slow-moving inventory, and/or review systems in place for planning/stocking inventory levels, demand planning, or procurement strategies (which may be leading to excess inventories).

If, in this example, the company’s receivable C2C exceeded industry standards, the company would have identified and implemented strategies such as speeding up the invoicing process, reducing billing errors, quick identification of slow-paying customers, improving the credit approval process, or any number of effective techniques.

Similarly, had the A/P C2C been out of line, actions could quickly be taken, such as review and negotiation of payment terms with key suppliers, matching payment of key purchases to related revenue buckets, vendor managed inventory and more.

However, it is important to note that being too aggressive in this A/P area may endanger the supplier relationship and, therefore must be a reasonable and balanced approach. This is because the supplier should be attempting to use C2C to balance the cash cycle as well.

The best results overall will be obtained when the entire supply chain is optimized and balanced among the company, its suppliers, and its customers, as to the cash-to-cash cycle. In this sense, as each player strives to improve its cash cycle, everyone “wins” when the Extended Value Stream is not destroyed, but achieves a balanced steady state.

As in any continuous improvement program, the company should then capture and report, as part of its monthly operational reporting, the cash-to-cash cycles for inventory, A/R, and A/P. If the strategies elected and implemented to improve the cycle time are successful, the results will be evident in trend analysis moving forward.

In addition, the company could continually benchmark its improving C2C cycle days with industry and competitor norms – which also may be improving – to assess the company’s competiveness on a dynamic basis.

As improvements are realized in the form of lower C2C days, continuous efforts should be made to compare performance and determine new opportunities for improvement. In this way, it is apparent how the management of the cash-to-cash cycle and continuous improvement go hand- in-hand to achieve improved performance within a business or organization.

Linking C2C to Supply Chain

C2C cycle management also dovetails to lean thinking when considering the company’s entire supply chain – driving inventory-based decisions for itself and for its customers. If the company’s inventory lean planning practices drive down required inventory investment to “what the company needs,” “when they need it,” and “how they need it,” then the same can be said for planning finished good deliveries for the very same criteria from the customer’s perspective. Success in these strategies drives down inventory and decreases the number of days that it is tying up cash resources, thereby manifesting itself in lower inventory C2C days. Those companies that excel at such practices will, in C2C terms, increase the speed at which cash cycles through the business process, reduce the need to rely on line of credit borrowing, reduce interest expense, improve liquidity and lower the company’s cost of capital.

In the simplest view, focusing on improving the C2C cycle enables the “linkage” of both operational and financial measures to drive toward excellence. The key to this may lie in seeking an internal (company) “balance” between the resources deployed in strategies to improve the cycle, versus the working capital required to achieve a “steady state” with the company’s suppliers and customers.

In the broadest view, C2C may be used to evaluate how an inventory decision, for example, may impact a company’s liquidity. In this sense, one decision may require increases in inventory to achieve a desired service level, but it may also elevate the demand on liquidity (cash resources).

On the other hand, decisions to decrease inventory levels will reduce C2C days and, thereby, decrease liquidity required otherwise for operations.

In a similar way, by evaluating supply chain strategies, cash-to-cash may be easily employed to determine the impact of alternate improvement ideas. This will put them on the same “playing field” in terms of days in cash, thereby making them comparable. Furthermore, this can be done in modeling assumptions during future periods over which effects on cash may vary but result ultimately in improved cash utilization, as shown in C2C metrics.

C2C cycle measurement may be beneficial in formulating the strategic planning of maximum possible profit levels with a range of planned operations, as C2C targets become embedded in the assumptions behind targeted inventory levels within constrained cash/borrowing limitations.

Also, while planning to target business market valuation levels (to be attained), C2C targets can also be used; lower C2C cycles correlate to higher net present value of cash flows from deployment of assets, and thereby to higher enterprise value. This may be useful in longer range strategic planning for build-to-sell or various exit strategies.

In summary, C2C cycle measurement offers a very simple and versatile tool to employ in strategic planning and continuous improvement for both product-based and service-based companies. It also enables a company to measure the results of targeted operational and financial improvements – not only in terms of how efficiently it uses cash in the deployment of its chosen strategies, but also in terms of how it performs in the marketplace versus the competition.

Regardless of the industry or of the improvement strategies employed by a company, C2C cycle measurement offers a comprehensive, easy-to-use method of tracking real improvements in terms of the best common link in business today: cash.

4.2 Reduce (Improve Return on) Fixed Assets

The Network

As companies continue to expand their global reach, supply chain complexity and risks significantly increase. Rising labor and fuel costs, political instability of offshore locations, erratic economic conditions, increasing regulations, the possibility of a merger or acquisition, and new competition (especially from offshore competitors) have put companies in a constant struggle of maintaining or improving customer service. At the same time, reducing costs and increasing productivity in their supply chain networks in a critical strategy.

While the impact of supply chain performance on the bottom line and shareholder value is increasingly well-understood, many companies have not changed their supply chain networks to keep up with new demands, including the demands generated by a new and growing consumer market in China.

With such turmoil, companies realize that they must reinvent their supply chain networks in order to remain competitive. In fact, given the recent recession, some organizations have already made modifications to their supply chain networks.

Others are scrambling to reinvent their supply chain networks in order to better use existing infrastructure, resources and working capital while allowing for growth and change.

However, reinventing a supply chain network is a time-consuming and daunting challenge. It requires a deep understanding of all aspects of the current supply chain and a comprehensive analysis of detailed operating data, along with many external factors, such as market forecasts or new channels of business.

Supply chain network planning is the process by which companies restructure their supply chain network in order to find the right balance between costs (manufacturing, warehousing/ distribution centers, transportation and inventory) and customer service.

Given the size of the challenge, most companies usually tackle network redesigns as “one time” events undertaken every three to seven years, often triggered when network costs get too great or by a major event, such as a merger or a change in supply chain strategy.

While there are a number of ways to approach the network planning processes, it is usually done with commercially available network modeling software.

These tools provide the capability to examine dozens or hundreds of options that are difficult to do so otherwise. There are two main types of planning tools:

-

Optimization Tools

-

Network Planning and Optimization – used to design the “optimal” network of facilities by balancing the tradeoffs between costs and customer service

-

Inventory Optimizers – used to identify optimal inventory deployment by facility and policies for a given network of facilities

-

-

Simulation Tools – used to evaluate how real-time variability can impact supply chain performance and risk

The typical network planning exercise is done in two phases:

-

Optimize the structure of the network.

What is the number of facilities, their locations and sizes, and what are the transportation modes and lanes to optimize the total network costs?

-

Optimize the inventory once the network structure is defined.

What is the right inventory at each location in order to meet the desired service levels?

Typical questions answered by supply chain network planning include:

-

How should the network expand or retract to optimally service present and future demand?

-

How many plants and warehouses should exist? What are their sizes, locations and capacities?

-

How many distribution centers should exist? What are their roles, sizes, locations and capacities?

-

Where should inventory be stocked, in what quantities and at what costs?

-

What transportation modes and lanes are best to move products through the network and, ultimately, to customers?

-

Which customers and products should be served from each facility?

-

How much capacity will be needed at each plant or distribution location?

-

As a result of a recent or proposed merger, what would an optimal, combined supply chain network look like?

-

What lead times should be offered, and what is the impact on service level?

-

What is the impact of sourcing from various suppliers?

-

What are the best ports of entry to use?

Supply chain network realignment can result in substantially improved networks that save millions in total supply chain cost – often anywhere from 5% to15%. But network realignment also results in customer service benefits of improved order fill rates, reduced order cycle times, and better customer relationships.

In the past, network planning has usually been focused on the strategic process of establishing the optimal network structure through closing and opening facilities. Once the network is established, most companies then stop the process until the next event causes the process to start all over again.

While most companies will not redesign their network structure on an ongoing basis, more are using the process to find better ways to support near-term planning decisions in order to leverage existing networks for more immediate gains.

Companies are beginning to look at their supply chains as a way to maximize profits and gain returns on capital or assets rather than just from a “cost minimization” perspective. This is a much different focus and requires significantly different thinking than solely minimizing supply chain costs.

It means that companies need to assess issues such as:

-

Which suppliers should be used?

-

What are the most effective go-to-market strategies?

-

What SKUs are the most profitable?

-

When does it make sense to drop a SKU?

-

Which customers are the most profitable?

-

When does it make sense to raise prices for a customer or to drop them altogether?

-

What is the best flow for new product introduction?

-

How should inventory policies be adjusted during product lifecycles?

-

What are the best transportation strategies to deal with fuel fluctuations?

-

How should inventory be redeployed if fuel costs continue to rise?

-

When do product postponement strategies make sense?

Successful network design will always come down to the specific needs of the business, the needs of the customers, and the types of products moving through its veins. Reinventing the company’s supply chain network is beneficial, whether the company wants to minimize costs, improve customer service, maximize profits, minimize capital outlay, or make sure processes are efficient.

With some experiencing a 50% improvement level on return on investment (ROI), companies that have not recently assessed their network design should make doing so a top priority goal.

Technology

The world of supply chain technology is more challenging than ever today – faster pace of evolving business process requirements to drive higher productivity and customer service enhancements; increased budget constraints; and expensive, aging legacy software and hardware architectures. All of these challenges can negatively impact supply chain value creation if not properly managed with an eye toward tactical efficiency, as well as an eye toward the emergence of new technologies (especially in Asia).

From a tactical efficiency perspective, upgrades to existing supply chain execution software applications and underlying technology stacks must be addressed in the next 12-24 months. Many organizations are running supply chain applications that have seen limited to no upgrades since they were installed circa 2002-2006.

During that period, many organizations continued to adapt and improve operations, leveraging as much functionality as possible out of the older supply chain technology platforms.

However, as the clock ticks on these older platforms, the cost to maintain the systems and risk of obsolesce only grows. At some point in the very near future, these organizations are going to face the prospect of a potentially expensive upgrade.

Figure 6 shows standard technologies being used by supply chains.

Figure 6. A Supply Chain Technology Platform