Applying Demand-Driven Practices to Reduce Lead Times

Gene Tyndall

EVP

Tompkins International

Doug Kane

Industry Partner HighTech and Manufacturing

One Network Enterprises Inc.

February 2013

Introduction

The consumer electronics industry is characterized by high degrees of new product introduction, relatively short product life cycles, supplier variability, high levels of competition, and required speed to markets. Companies producing or selling consumer electronics products must compete not only on the price, quality, and features of their products, but also on related customer service strategies. Developing appealing products is essential, but if they are not supplied to customers when, where, and how they want them, electronics manufacturers and distributors will underperform.

Supply chain capabilities are key to delivering on the consumer electronics industry’s value proposition (i.e., why customers will buy our products). Supply chains must provide the right products, to the right places, and in the right quantities, or sales will be lost, and operating margins will be limited.

The Value Drivers of Consumer Electronics Supply Chains

Similar to other industries, the supply chains of consumer electronics companies are optimized by best dealing with three value levers:

-

Demand Variability

-

Supply Variability

-

Lead Time

A company’s ability to respond rapidly to the variability of demand, and match it with supply, is the top factor in determining the effectiveness of its supply chains – and its operations. The consumer electronics industry has unique drivers that cause major differences in the amplitude of these three levers.

Competing companies are subject to similar demand/supply variability. They also have similar physical lead times from raw material/component suppliers on the supply side, as well as from logistics providers on both the supply and demand side. There are, however, unique operating strategies that companies can employ to reduce variability (e.g., demand shaping, VMI, global hubs, postponement, etc.). This paper addresses the issue of lead time – defined as the time it takes for components or materials to flow from their origins in the supply chain to customers as finished products.

First, a few definitions:

Total Supply Chain Time: the total calendar time required for a company to spend money (BUY) and to collect money (SELL) for a given product

Total Cycle Time: the total calendar time required for any given cycle of a supply chain (e.g., purchase order for component to delivery, assembly plan to actual, customer order to delivery, procure to pay, etc.)

Order to Delivery: the calendar time required for a customer order to customer delivery

Actual Lead Time: the calendar time for components/materials to flow from supply chain origin to customer or consumer receipt

System Lead Time (sometimes referred to as systemic lead time): the calendar time required by business processes to get the right products to the right places at the right times

The Anatomy of Actual Lead Time

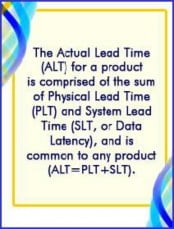

The Actual Lead Time (ALT) for a product is comprised of the sum of Physical Lead Time (PLT) and System Lead Time (SLT, or Data Latency), and is common to any product (ALT=PLT+SLT). Any company that acquires raw materials or components for a manufacturing process, then produces and distributes its finished products, must deal with ALTs.

A company’s value is enhanced when it produces and sells product at the highest service level and the lowest total cost. When a company minimizes its ALT, value is created. Since PLT is the amount of time it takes to physically move components or materials from one stage to the next, PLT is mostly fixed (depending on the physical network of facilities). Thus, the ability to reduce the variable lead time creates significant decreases in inventory levels, as well as important increases in customer service levels, onshelf availability, and readytoship statuses. All of this increases sales revenues.

SLT is the aggregate amount of time (weeks, days, hours and minutes) required to respond to actual realtime consumer demand signals. Until recently, without technology support, most operations processes have been manual and timeconsuming. For example:

-

When a retail store is running low on inventory, it issues a replenishment order to its Distribution Center (DC). This request may require phone calls, emails, faxes, or complicated Electronic Data Interchange (EDI) orders to be issued and confirmed. The DC then accepts the full order with a scheduled delivery (if it has inventory) and replies back to the retail store by similar channels. If the DC has sufficient inventory to fulfill the order, the lead time is a minimum of one day, but often it is longer. If the DC does not carry the inventory to meet the order, it then places an order on the manufacturer’s DC, requiring several more days for ALT. All this time may impact revenues, and it certainly impacts operations.

-

If it is a completely manual system, then it requires phone calls, emails, faxes, or followup phone calls from the retailer’s DC to the manufacturer’s DC and similar messages, including checking transportation availability, etc., just to respond. This process requires substantial time, even with the use of EDI. There is at least another day of SLT, unless the manufacturer DC does not have enough inventory to fulfill the DC order that is trying to fulfill the retail store order. Again, loss of revenues and increased operating costs occur for both parties.

-

These same events occur all the way “up the chain” with suppliers, distributors, and other trading partners, which may well involve hundreds of component producers.

SLT is a significant part of the ALT for any company. Gartner Research, for example, has estimated that up to 40% of ALT in a supply chain is due to SLT.

The figure below illustrates the traditional supply chain with its serial actions by multiple trading partners.

The negative effects of SLT expand significantly the further down the value chain it propagates. The net effect is that companies need to build excess inventories or safety stock to react to orders and maintain service levels. Since up to 40% of ALT is made up of SLT, it can be surmised that SLT creates up to 40% excess in supply chainwide inventories, across trading partners involved in that product category.

Why Does System Lead Time (SLT) Remain a Problem?

Most companies have invested heavily in information technology – Enterprise Resource Planning (ERP) and supply chain – in an effort to optimize individual business processes, with varying degrees of success. These investments have led to massive point solutions, ranging from Excel spreadsheets to multiple different demand planning and supply chain planning tools that are loosely integrated (if at all) at the enterprise level.

When considering trading partners outside the “four walls” of any enterprise, the problem only gets worse. Multiple systems and multiple IT platforms create huge integration challenges and risks. Technology expansion efforts fail to resolve the problem, because the underlying architectures and data models of most current systems are not flexible enough to accommodate the multiparty, multiechelon supply chain structures that exist between customer demand, manufacturers and all supply trading partners.

ERP suppliers have had some success in creating data repositories that allow manufacturers to execute material plans and provide automated financial accounting in the execution of those plans. ERP systems and their fixed data models, however, force companies into the ERP suppliers’ predetermined processes. The limited flexibility of these architectures makes it impossible to meet the requirements of implementing endtoend, multitier, and multiparty demanddriven supply chain strategies.

Many point solutions evolved from the limitations of ERP. Memory resident “fast MRP” systems allow companies to extract ERP data and run faster “what if” analyses, with some value as decision support tools. Further, supplier collaboration tools evolved as a way to give some visibility and interaction between companies and their suppliers.

Demand planning and translation tools have offered a level of value, as have TMS and WMS solutions. Yet the lack of integration, both inside and outside the four walls of an enterprise, has done nothing to minimize SLT, and, in fact, has often added to SLT.

How to Reduce or Eliminate SLT

In an ideal world, actual realtime consumer demand and its effects would get propagated and shared, and acted upon, across the supply chain, instantaneously. With the limitations of commonly used technologies stated above, it is clear that a new stateoftheart solutions architecture is required.

Such a platform must be flexible and allow each company in the supply chain to implement its own processes, without requiring every company to use the same processes. Most important, it should enable unlimited numbers of trading partners to plan, execute, monitor, synchronize, and optimize in real time all of the business processes and events that take place throughout complex, multi-echelon trading partner ecosystems – from consumption points through raw material suppliers

The system also needs to have several underlying technology pillars in order to respond to realtime customer demand data:

-

Anytoany, multi-echelon networkbased architecture: Companies trade with multiple parties in their demand/supply communities. Multiple companies in an industry do business with many of the same trading partners in these demand/supply communities. Onetomany architectures fail because they require multiple logins for a supplier or a customer to interact with all of its customers or suppliers in that industry. Without multiparty and multiechelon, it is impossible to model the tiers and complexities of all the different interactions between companies.

-

Best-of-breed capabilities and a single version of the truth: As actions move across endtoend supply chains, interactions between companies on differing systems (often times in their own company) require an architecture that provides for both best-of-breed application functionality and a “single version of the truth” throughout the cycles. Business processes, and planning and execution systems, vary from company to company. A system architecture that allows individual companies to define their own processes and interact with the processes of others in the supply chain company is critical.

It is also important to be able to define different systems of record as transactions move through the process. As an example, an order from a retail DC may be executed by an SAP system and sent to a manufacturer that accepts and replies to that order on another system. An architecture that provides for both a single version of the truth and best-of-breed capabilities based on any customer’s unique processes will alert all parties in real time, and in each party’s unique information format, that an order has been replaced. It also allows the manufacturer DC to respond and execute, provide its status, execute the process, and once reconciled, the next action can begin.

-

Continuous and incremental re-calculation of requirements tied to execution: Actual demand must be monitored continuously. As changes occur, the system must trigger planning and execution processes to optimize the demand/supply match immediately. Continuous tracking is crucial for sensing changes in demand or supply. Only those trading partners whose operations are affected by changes to demand, supply, asset availability and capacities are notified, and operations are redirected automatically and instantaneously as required.

-

Advanced sense and respond (real-time sense with real-time automated response): Many solution providers claim to have real-time sense and respond capability. However, what they do not say is that their sense and respond technology can sense a change but the response is nothing more than an email or alert telling the users that something has changed. To achieve optimal supply chain performance, the system needs to sense changes in real time as well as provide intelligent optimization capabilities that automate and execute the optimal response where possible under the constraints of the business. Only when an automated optimal response is not possible should the appropriate user be alerted that they need to get involved and provide a manual response.

-

Scalable/flexible architecture that is easy to deploy: Look for a system that will scale to any number of tiers or echelons within a supply chain. An architecture is required that has the flexibility to quickly model the most complex supply chains and to provide continuous and incremental planning tied to execution.

A Cloudbased architecture that is easy to deploy is critical, especially for companies that are exhausted by long drawnout and costly ERP implementations. An architecture with these characteristics enables companies to deploy more modern capabilities in stages. They can simply access different functionalities when they are ready for the next phase of implementation. With ERP, the return on investment takes years to achieve if at all. However, an architecture than can be deployed in distinct stages brings immediate and incremental value at each stage. This not only shortens a company’s time to create value, but each stage will fund the subsequent stage, allowing for a self-funding deployment.

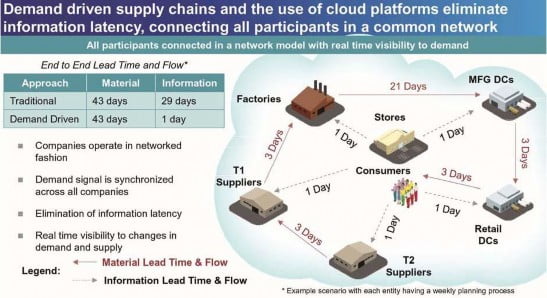

The figure below illustrates the demanddriven replenishment chain, operating in networked fashion.

Without these five technology pillars, it is impossible to fully eliminate SLT, and it is extremely difficult to reduce it. With all activated, SLT can be completely eliminated as part of a demanddriven value chain operations strategy. When a realtime demand signal is sensed, only a system based on the technology pillars described above is capable of automatically propagating the necessary actions, calculating the effects of demand and supply signals upon the entire supply chain, and automatically executing the optimal response in order remove or minimize SLT.

The Demand-Driven Operations Strategy at Work

ALT can be reduced to either be equal to, or nearly equal to, PLT by the use of demanddriven supply chain operations strategies implemented on a technology platform that includes all of the necessary technology pillars. When there are longer ALTs, companies and their supply chain partners carry higher excess inventory levels. If SLT for any company is 40% of its ALT, then its inventory levels can be reduced by at least 40% through implementing demanddriven operations, business processes, and the right technologies.

Consumer electronics companies benefit from demanddriven solutions as much as consumer packaged goods companies and others. For example:

-

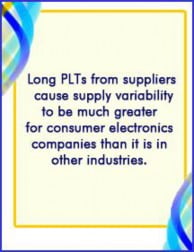

Long PLTs from suppliers cause supply variability to be much greater for consumer electronics companies than it is in other industries. With ALTs being so backend loaded and heavily reliant on suppliers’ abilities to deliver, accurate forecasting is a critical component in optimizing supply chains. Due to this reality, many consumer electronics companies have invested heavily in supplier collaboration and other tools focused on statistical forecasting/demand planning in conjunction with ERP solutions.

-

Integrated Business Planning (IBP), with demanddriven S&OP is a crucial part of consumer electronics products success. Both One Network and Tompkins International have published position papers on this topic:

-

Demand Driven Sales and Operations Planning, January 2012

-

DemandDriven Supply Chains: Getting It Right for True Value, February 2012.

-

Sales & Operations Planning in Manufacturing: Manage Collaboration Across the Entire Organization, February 2012.

-

Supply Chain Priorities for the HighTech Industry: Top Seven Success Factors for Value Creation, September 2012.

-

-

Because of the investments in inbound supplier collaboration and ERP to standardize manufacturing operations, unlike other industries, consumer electronics companies have minimized the value of realtime demand data. For example:

-

Most consumer electronics companies manufacture a large percentage of their products in Asia. Many build their critical electronics (populated PC boards) in modules in Asia and move these to final assembly locations in the US and other customer markets around the world.

The products or components are transported around the world in containers on ocean carriers and intermodal means, which require up to three weeks before they arrive at the DCs or final assembly plants.

By minimizing actual consumer demand data, each one of these “floating warehouses” is carrying product based on production schedules that are locked for 30 days. As containers are filled and launched, a company is committed to that inventory. In today’s push environment, a shift in actual demand versus forecast demand has the effect of the company building the wrong inventory and loading up an expensive floating warehouse that commits the company to that inventory.

By sensing realtime demand data with a continuous incremental recalculation run through the optimization process, it is possible to continuously and incrementally modify operational execution (subject to contracts and constraints) to ensure that each floating warehouse contains the optimum product to meet demand. The net effect is that the arriving product will be better matched to consumer demand, thus minimizing excess obsolete inventory that must be sold at a discount or written off completely.

-

Beyond supplier collaboration on plans, it is critical for consumer electronics companies to have visibility into supplier constraints, Available to Promise (ATP), workinprocess and finished goods inventories. SLT can be eliminated by combining realtime demand with continuous, incremental planning and execution that has integrated visibility into supplier inventory and supplier/logistics capacity. As stated earlier, demanddriven supply chain processes, supported by the right technologies, can optimize flow based on actual demand while subject to supply and logistics constraints. Without any human interaction, product built to an optimized accurate forecast is immediately accessible to users, at the lowest possible total delivered cost.

-

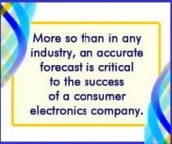

The demanddriven solution for consumer electronics is very exciting and attractive. Long supplier lead times significantly increase the supply variability in relation to other manufacturing companies in different industries. Consumer electronics manufacturers have invested heavily in ERP and supplier collaboration tools in an effort to minimize supply variability. Yet, more so than in any industry, an accurate forecast is critical to the success of a consumer electronics company.

Demanddriven operations should replace the overfocus on supplier availability. This will enable consumer electronics companies to roll up all the forecasts for all products in all channels and create a single sales plan. From that sales plan, all operational plans – including those for materials, manufacturing, distribution, and finance – are automatically generated with more reality. The highest possible forecast accuracy can be achieved by integrating realtime demand data that will allow for continuous and incremental planning and execution, on a daily basis. Inbound supply can be matched very closely to actual demand, subject to supply constraints. Since the system will be sensing and responding continuously and incrementally, SLT will be eliminated. Thus, consumer electronics companies can finally optimize/minimize inventories throughout their end-toend supply chains.

The Right Path Forward

Getting on the right path toward demanddriven supply chains is not difficult. The Tompkins International and One Network joint solution starts with a relatively brief assessment of the current supply chain for consumer electronics to determine the “ASIS” current state. The assessment examines operations strategy, business processes, technologies, and performance measures associated with the demandsupply product flows to determine the potential value present in gaps and opportunities.

Assessing the ASIS current state and determining the steps needed to achieve the value will reveal the full value proposition (i.e., the net improvements to be gained from converting to the DDSC). The Tompkins/One Network approach is to prove this value by carrying out a pilot test of the adjusted operations strategy, processes, and technology, for one product category. This pilot normally requires about 90 days and serves to prove the value proposition.

The One Network technology is Cloudbased and operates as Platform-as-a-Service (PaaS). This reduces integration, testing and implementation to a small fraction of the time that is required to implement ERP systems and technologies that involve large integrations and data file conversions. Strategy and process changes are also relatively straightforward, since the demandsupply business processes are simplified. Often the most challenging practices are those involved in change management.

Summary and Conclusion

This paper unveils the significant positive financial improvements that are achieved when eliminating SLT through the implementation of demanddriven supply chain operating strategies – via the right processes and the right technologies. When the right technologies are employed on a platform based on the five technology pillars, and the business processes are aligned to enable effective execution, SLT is eliminated and inventories are significantly reduced for any manufacturing company. This is also true for its trading partners in any product supply chain.

Moreover, there is substantial value through improved demand forecasting that is driven by actual sales on a near realtime basis. Continuous and incremental planning tied to execution turn operations toward demand-driven principles, and less toward supplydriven. Integrating actual demand data enables the optimal matching of demand and supply, subject to supply constraints. Fewer sales are lost and service levels increase – all with lower operating costs.

At the end of this paper is an example of a company that has two products (PC1 and PC2). This example illustrates the effects of data latency on product mix, inventory levels, and customer service levels (stock outs/missed revenue opportunities).

Below are other demanddriven operations strategies that may be employed by consumer electronics companies:

-

Postponement and personalization strategies that can only be deployed with the technology architecture discussed in this paper.

-

Optimizing product distribution and deployment through integrated realtime demand data and lastminute allocation.

-

Optimizing logistics, including load optimization, aggregation, zone skipping and other strategies.

-

Minimizing inventory costs and optimizing final assembly through VMI and/or hubs.

These strategies perform highly with the right technology and the right business processes. In future papers, Tompkins International and One Network will outline how these are best implemented and enabled.

About Tompkins International

Tompkins International transforms supply chains to create value for all organizations. For more than 35 years, Tompkins has provided end-to-end solutions on a global scale, helping clients align business and supply chain strategies through operations planning, design and implementation. The company delivers leading-edge business and supply chain solutions by optimizing the Mega Processes of PLAN-BUY-MAKEMOVE-STORE-SELL. Tompkins supports clients in achieving profitable growth in all areas of global supply chain and market growth strategy, organization, operations, process improvement, technology implementation, material handling integration, and benchmarking and best practices. Headquartered in Raleigh, NC, USA, Tompkins has offices throughout North America and in Europe and Asia. For more information, visit www.tompkinsinc.com.

About One Network Enterprises

One Network Enterprises Inc., a high growth technology company, provides the world’s first enterprise networking platform that exploits the latest principles – mobile apps, social networking, cloud-based computing – that are revolutionizing consumer technology. Known as the Real Time Value Network, this unique and revolutionary platform is used today primarily to drive dramatic improvements in demand, supply and logistics management effectiveness and efficiency. All of the stakeholders in any trading partner community have access via this platform to timely and accurate information, and a “single version of the truth,” regarding changes in demand and supply conditions. This enables trading partners to plan, execute, monitor, synchronize and optimize in real time all of the business processes and events that take place throughout their extended supply chains. The Real Time Value Network currently serves a pre-existing community of more than 30,000 trading partners.

Contact

Gene Tyndall

EVP Tompkins

International

gtyndall@tompkinsinc.com

Doug Kane

Industry Partner, High-Tech and Manufacturing

One Network

dkane@onenetwork.com