Food Fight

Discovering Eight Truths of the New Era of Retail

By: James A. Tompkins, Ph.D.

1.0 INTRODUCTION

On June 14, 2017 I gave the keynote at the EyeForTransport Supply Chain Summit in Chicago. The Topic was “Avoiding the Supply Chain Treadmill”. In this presentation I discussed how we all must avoid the “business-as-usual” trap of continuous improvement and be ready for major disruptions occurring in our supply chains. I gave a specific example regarding the upcoming upheaval to occur in the US grocery business. The next day, June 15, 2017 at the same conference I made a presentation titled, “Reacting to and Riding the Wave of the Amazonification of Industry”. In this presentation I highlighted the tremendous success of Amazon and cautioned that I believed the pace of industry disruption was going to increase and that nothing Amazon would do would surprise me. By 10AM on June 16, 2017 I started receiving emails regarding Amazon’s purchase of Whole Foods. My reaction was quick and clear:

-

Good move on Amazon’s part.

-

Not at all surprising, this Amazon acquisition had been suggested in the news several times in the last several months.

-

As I predicted two days earlier, a major disruption in US grocery has now occurred.

-

As I predicted one day earlier Amazon’s pace of disruption had just accelerated.

-

I need to write a paper, “Food Fight: Amazon Eats Whole Foods for Breakfast”.

Interestingly, what did surprise me was the volume of discussion/analysis of this acquisition and the drivel that flowed from so many directions. In fact, after some travel and then catching up on July 4, 2017, I finally got ahead of the rubbish avalanche and began to write this paper. However, over the 25 day period from June 16, 2017 to July 10, 2017, I had received over 100 Amazon/Whole Foods articles sent to me by my research staff. Reading these 100+ articles concerned me as it indicated, not only did the press not fully understand what was happening with Amazon/Whole Foods, but they were publishing information that was not well founded. Below is a list of some of the articles that were not judicious:

-

The transaction would be upset by Kroger and Wal-Mart bidding a higher price for Whole Foods to keep Amazon out of Brick & Mortar or by the FTC for Anti-trust reasons.

-

Amazon’s goal in the transaction is to reduce Whole Foods S, G, &A, thus reducing costs and turning Whole Foods into a profitable low cost grocer.

-

Amazon is going to deploy their Amazon Go technology at the 460 + Whole Foods stores to claim market share from Wal-Mart and Kroger.

-

Amazon now has the needed logistics infrastructure and local fulfillment infrastructure to make Amazon Fresh successful.

-

Amazon is going to deploy their strong logistics expertise and turn Whole Foods into an online grocery juggernaut.

-

Amazon buying Whole Foods validates that eCommerce will never be substantial and even Amazon sees that Brick & Mortar is superior to eCommerce.

-

The Whole Foods organic business model is unique and will allow Amazon Fresh, Prime Now, Prime Pantry, Amazon Go, and Amazon Fresh Pickup exposure to a new customer base.

-

This transaction was not about the grocery industry, but about Amazon vs. Alibaba vs. Apple and their voice enabled speakers.

-

The Whole Foods stores will be used as drone delivery launch pads

-

The acquisition of Whole Foods by Amazon is not a big deal as it is about two small players in the grocery industry.

As I began to write the “Food Fight” paper debunking these stories it occurred to me that a more useful paper would be to use today’s “Food Fight” discussion as a way to exemplify the eight major new retail truths of retail success. It is my hope that this approach will allow you to understand not only the brilliance of the Amazon acquisition of Whole Foods, but also where retail is headed. The following eight sections of this paper cover the eight retail truths listed in Figure 1. Please note the term “retailer” in this paper refers to any company that sells to customers. A firm may think of themselves as a wholesaler, distributor, manufacturer, brand, eCommerce company, consumer package goods, etc, but if they are selling online, in-store, via mail, through television advertising, by catalogue, or in any form to an end customer, I will refer to them as retailers.

Figure 1: THE EIGHT MAJOR RETAIL TRUTHS OF RETAIL SUCCESS

-

Retail is broken and major disruptions are to be expected.

-

Success going forward in retail will require hustle and grit.

-

Post clique logistics is a big deal.

-

It is not about Bricks vs. Cliques, it is about Bricks AND Cliques.

-

Retail aggregation precludes retailers from being successful.

-

Unique is exciting and marvelous, common is dull and unpleasant.

-

Data, information, and insight are precious.

-

Do not be afraid to kill sacred cows.

2.0 RETAIL IS BROKEN AND MAJOR DISRUPTIONS ARE TO BE EXPECTED

2.1 FOOD FIGHT

Over the past 20 years many retailers have had the dream of entering the food retail business. The appeal is undeniable, huge revenues, repeat business, and in-store traffic. The fascination has resulted in a proliferation of food retail models ranging from dollar stores, off-price stores, convenience stores, drug stores, supermarkets, discount supermarkets, premium supermarkets, farmers markets, restaurants, online retailers, specialty/natural food stores, supercenters, and warehouse clubs. The appeal and fascination fades when the reality of low margins, a shameful amount of waste, and slow sales growth all set in. Even of greater concern is the lack of consumer loyalty in that every month 68% of Americans shop at five or more types of food retailers. In addition, the low margin struggles are getting worse as a result of:

-

Food retailers investing in technology and eCommerce.

-

Food retailers investing in-store and labor upgrades to delight the consumer.

-

Marketplace pressures to reduce food prices.

-

Food retailers getting into a “price race to the bottom”, “Food Fight” in order to not lose market share.

The results of these low margin struggles have turned the dream of entering the food retail business into a nightmare as illustrated by the following:

-

19 US grocers have filed for bankruptcy over the past three years.

-

Prices paid for groceries in the US have fallen for 17 straight months.

-

In the first quarter of 2017, sales of US food retailers fell 2.5%.

-

Kroger ended a 13 year streak of rising same-store sales in the first quarter of 2017, and then in the second quarter they fell again reporting that increasing competition will hurt earnings for the year.

-

Wal-Mart opened their first supercenter in 1988 and 14 years later they reached #1 on the Fortune 500 list, but in the 2017 Consumer Reports of Grocery Shopping Satisfaction ranked the top 62 grocers, Sam’s Club was ranked #39 and Wal-Mart was given the lowest ranking at #62.

-

Whole Foods has not been doing well.

-

Whole Foods has lost almost 50% of their market value since 2013.

-

Whole Foods has posted seven straight quarters of sales declines at established stores.

-

Whole Foods prices are reported to be 20-30% higher than most mainstream grocers, often referred to as “Whole Paycheck” because of the sticker shock at checkout.

-

However, John Mackey, Founder and CEO of Whole Foods, upon signing the Amazon agreement and retaining his CEO position while receiving a 26% premium for his stock, declared, “The deal is amazing for consumers.”

-

-

New discounters are entering the market exerting new market pressures.

-

Aldi: Plans to invest $5 Billion over the next five years to open nearly 900 stores bringing their US total store count to 2,500 by 2022.

-

Lidl: Opened their first ten US stores in June, 2017, expecting to open 20 more during the summer of 2017, and a total of around 40 stores in 2017.

-

-

From Webvan to Amazon Fresh and now Instacart, all have failed to create the sort of seamless buying experience we enjoy and expect with nonfood eCommerce.

-

Selling fresh, refrigerated, and frozen online is a real challenge.

-

Online food retail is only 2% of all grocery and it is not expected to hit 3% until 2021.

-

Online grocery orders are less profitable than in-store grocery orders.

-

With the above market dynamics in grocery and the turbulence food retailers have experienced, there is no doubt that food retailing is broken. Now, with the acquisition of Whole Foods by Amazon the major disruptions in grocery are just now going to begin. I believe food retailing has hit a tipping point where rapid change should be expected.

2.2 RETAIL TRUTH

The acquisition of Whole Foods by Amazon will not only have a huge impact on food retailing, but due to Amazon being the “Everything Store” and being the “Everything Company” with Amazon Web Services, Fulfillment By Amazon, Amazon Prime, and a significant assortment of Private Labels, this Whole Foods acquisition will have a huge impact on all retail. Although there are many lessons to be learned from grocery to non-grocery retail, one needs to be aware that with the margins in food retailing being substantially lower than in non-food retailing, what is true in grocery may or may not be applicable to non-food retailers. In fact, the M&A activity of the retail Titans (Alibaba, Amazon and Wal-Mart) presents an interesting view of how retail is being disrupted.

Consider:

-

Since 2015, Alibaba has invested more than $9.3 billion in physical retail stores.

-

In the last year Wal-Mart has spent over $4 billion buying eCommerce companies, the latest Bonobos, announced five minutes after the Amazon acquisition of Whole Foods.

-

Amazon has closed on 30 acquisitions over the last eight years spending more than $20 billion. Interestingly, after averaging over four deals a year for eight years straight, Amazon has only done two deals (Souq.com and Whole Foods) since the end of 2015. When the Whole Foods deal is closed in the second half of 2017, it will increase the Amazon acquisition spending to over $33 billion.

There will be further discussion on this in Section 5.

In 2016 eCommerce grew the most ever in the US at 15.6%. Of this growth, 66% belonged to Amazon. Of all non-food retailers doing eCommerce in the US, due to the final fulfillment and delivery costs, only 10% are profitable on these online orders (see Section 4 for more on post clique logistics). As a result of retail being broken, an ongoing barrage of disruptions and many retailers not stepping up, through the first six months of 2017 we have seen a record number of 5,321 store closings and a record number of retail bankruptcies. In addition, in 2016 we saw store traffic down by 8% and in 2017 we are seeing the fewest number of new retail jobs. Interestingly, according to Jones, Lange and Lasalle (JLL), from 2010 to 2016 there has been nearly a 40% increase in retailer leasing activity for eCommerce, while traditional retail leasing activity is down almost 38% in that same time span. Just like for grocers with the above market dynamics, there is no doubt that retailing is broken. Now with the acquisition of Whole Foods by Amazon the major disruptions in retail are going to begin. I believe retailing has hit a tipping point where rapid change is to be expected.

3.0 SUCCESS GOING FORWARD IN RETAIL WILL REQUIRE HUSTLE AND GRIT

The leadership characteristics that will impact the success of food and non-food retailers going forward are no different from the characteristics of great retail leaders of the past and present. This topic is not split into food and non-food. To the contrary, in Section 5 when we do not talk about the leadership characteristics, but rather about the experience and expertise of today’s leaders, we will differentiate between Brick & Mortar experience and Technology/eCommerce experience and expertise.

There are many historical leaders we can study to learn about their leadership characteristics. Here, I selected from a historical perspective the most innovative retail leader of all time, Sam Walton.

From a present day perspective, once again it is not difficult to select the leaders most worthy of study, and that would be Jeff Bezos and Jack Ma. When studying Sam Walton, Jeff Bezos, and Jack Ma we see three very brilliant executives that have drastically different backgrounds, but who have a lot in common with respect to their leadership characteristics. After considerable study I have decided the two leadership characteristics that all three of these dynamic, wildly successful executives share are hustle and grit.

The word “hustle” is an interesting word as it has morphed from being a negative word into being a positive word. In the 1600’s the word “hustle” meant to force (someone) to move hurriedly or unceremoniously in a specified direction, as in “they hustled him into the back of a horse-drawn wagon”. In the 1700’s the word “hustle” meant to obtain by forceful action or persuasion, as in “they headed to New York to try and hustle a distributorship”. In the 1800’s the word became even more aggressive as “hustle” meant to con, swindle, fraud or cheat, as in “he got hustled in a card game and lost considerable money”. In the 1900’s the term “hustle” took an even worse path as it was often used to indicate being engaged in prostitution, as in “he was arrested for hustling”. From these negative connotations comes a very positive, complimentary use of the word “hustle” meaning to make something happen, to focus on a goal, and to move towards it. This modern use of the term evolves from the use of the term “hustle” on a basketball court meaning “scrappiness, toughness, high energy, and diving on loose basketballs”. It is this modern definition of “hustle” that I am using to describe Sam Walton, Jeff Bezos and Jack Ma. To “hustle” today is:

-

To have a strategy for benefiting from a fast-moving and uncertain world.

-

The most important tool of the “New American Dream”, in which we reassert power and control over the system owning our dream.

-

To have the skills, focus, speed and commitment to success, independent of challenges faced.

-

To be bold and not to avoid risk, but to manage risk.

The word “grit” is again a modern term where its meaning is:

-

Passion and perseverance for long-term goals.

-

The ability to remain unshaken in pursuit of objectives.

-

Stamina in the face of adversity.

-

Holding steadfast to goals even when there are bumps in the road.

It is my belief that entrepreneurship, innovation, and creativity demand “grit”. “Grit” is not about following a single course of action at all costs. To have “grit” means being flexible and seeing obstacles not as threats but as challenges, failures not as mistakes but opportunities to learn. As I think of another modern leader with “grit”, I think of Mark Zuckerberg, creator of Facebook, a quote attributed to him: “Fail Fast, Fail Often.”

As I think about the eight major retail truths for both food retailers and non-food retailers in today’s dynamic, fast-paced, often disrupted, and often unpredictable environment as described in Section 2, my wish for you is that you move forward with hustle and grit.

4.0 POST CLIQUE LOGISTICS IS A BIG DEAL

4.1 FOOD FIGHT

As will be covered in Section 4.2, post clique (after the customer places their order) delivery is extremely important to all eCommerce companies. For food retailers it is either the critical element, extremely important, or unimportant. Post clique logistics is the critical element when a customer is ordering fresh (Fresh) and the customer lives in a major urban center (Big City). Post clique logistics is as extremely important when we are restocking the pantry (Pantry Restock), it is unimportant when the customer orders Fresh and lives in small urban or rural area (Non-Big City), or for unique pantry (Unique Pantry). The segmentation is the beginning of the aggregation concept (refer to Section 6). I will not get too detailed on this yet and address the food categories Fresh, Pantry Restock, Unique Pantry, and delivery destinations Big City and Non-Big City.

Here are definitions:

-

Fresh: anything that requires temperature controlled delivery. This includes fruits, vegetables, meat, fish, dairy, frozen, and anything else perishable. Fresh is growing 5% each year, product velocity is essential as time delays diminish product quality.

-

Pantry Restock: 80% of all items purchased from a food retailer. The non-perishable items that customers buy consistently. This includes the customer’s favorite, non-perishable food, beverage, household & pets, beauty & grooming, nutrition, wellness & healthcare, baby care, etc.

-

Unique Pantry: Non-perishable, special purchase items that a customer has not purchased before and wants to interact with the product (possibly items like cake mixes, spices, new products, etc.).

-

Big City: At this point a large urban area where affluent people live who do not drive cars on a daily basis. Cities today that qualify are Atlanta, Baltimore, Boston, Chicago, Dallas, Denver, Los Angeles, New York City , Philadelphia, San Diego, San Francisco, San Jose, Seattle, Washington, DC, and in some cases adjacent surrounding areas.

-

Non-Big City: All locations in the US that are not Big City.

The importance of post clique logistics for these categories are:

-

Fresh Non-Big City: Only available for a delivery fee most people are not willing to spend.

-

Fresh Big City: Critical for folks who are willing to pay for delivery via a service like Amazon Fresh, Fresh Direct, Lyft, Instacart, Peapod, Shipt, or Uber and who are willing to allow others to pick their Fresh products.

-

Pantry Restock: Readily available, same as non-food eCommerce.

-

Unique Pantry: Typically a customer wants to do their own selection.

The largest challenge here has to do with Fresh. From one perspective customers do not desire delivery of their Fresh products as they want to be personally engaged with squeezing/thumping the fruit, selecting their vegetables, fish, meat, etc., for this reason the demand for Fresh delivery is limited. Secondly, Fresh delivery is very complex with special handling/temperature controls being required for apples, bananas, lettuce, tomatoes, eggs, dairy, etc. Thirdly, Fresh delivery must be done on a time definite schedule because the customer needs to be home for the delivery (you cannot just leave Fresh on the porch or give Fresh to the bellman). Lastly, delivery is very expensive as the time on the customer property is much longer with Fresh than on a non-Fresh delivery. It is for all these reasons that eCommerce delivery of Fresh is not a profitable pursuit unless the customer is willing to pay a significant fee for the delivery. There are essentially three categories of Fresh delivery services:

-

Deliver to a customer from a local fulfillment center: AmazonFresh, FreshDirect, and Peapod. Profitability for these services is a challenge and only possible in the largest most affluent Big Cities where over 25% of the households do not own a vehicle (New York City, San Francisco, Chicago, Philadelphia, Washington, DC, Baltimore, and Boston). A troubling concern with the growth of these services is a new demographic that has surprised many. In theory, for the decade from 2011-2020 Americans were supposed to flock en masse to cities. For the first five years of the decade this happened and then in 2016 the suburban population gains outpaced cities for the first time since 2010. If this trend continues growth plans for Fresh delivery may be unrealistic.

-

Personal shoppers who pick orders for a customer from a store (Whole Foods, Costco, Target, Harris Teeter, Publix, Safeway, Ahold-Delhaize, Wegmans, CVS, etc.) and delivers them to a customer, Instacart, and Shipt. Profitability for these services depends upon the revenue streams from the customer for subscriptions and fees, from retailers on revenue sharing basis and from CPG’s from promotions.

-

Local transportation firms who can deliver products from stores (Wal-Mart and Kroger) to customers for a fee, Lyft and Uber.

An interesting statement with respect to the Amazon acquisition of Whole Foods is that Amazon’s “expertise in logistics” will help Whole Foods with Fresh Delivery. There are two problems, first Whole Foods has four years left on a five year contract for Fresh with Instacart with whom Whole Foods owns an equity share, second Amazon is without a doubt a leader in non-perishable, from most reports they do not have Fresh expertise and are behind both FreshDirect and Peapod.

My view is the bottom line for the Amazon acquisition of Whole Foods to be successful:

-

Use the stores for customer shopping of Fresh, experiential purchases, beer, pizza, bakery, sushi, cheese, oyster bar, olives, barbecue spots, coffee roasting, prepared meals, in-store caf, Unique Pantry, etc.

-

Use the Amazon Fresh Pickup at Whole Foods Stores for curbside pickup of Fresh as desired by a customer.

-

Use Amazon Prime Pantry for Pantry Restock for either delivery to home or curbside pickup.

-

Use Amazon Lockers at all Whole Foods stores instead of delivery to home for pickup (as directed by customers) of general merchandise not available from Whole Foods.

4.2 RETAIL TRUTH

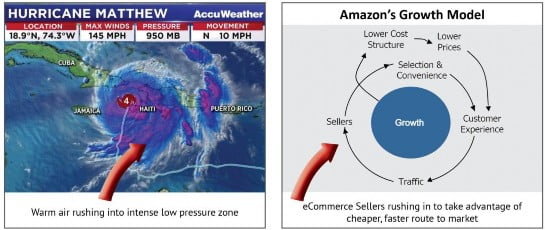

Clearly the US leader in non-food eCommerce post clique logistics collaboration is Amazon. Amazon has done an awesome job of free post clique logistics fulfillment and delivery. Amazon has altered customers’ expectations with respect to how quickly they expect to receive orders.

Take a look at the two illustrations contained in Figure 2. One illustration is one of the most powerful and potentially disruptive ecosystems known to man. The other is a category 4 hurricane.

Figure 2. Hurricane Matthew and Amazon’s Growth Model

In fact, both systems work in a similar way. The hurricane is driven by an intense low pressure zone created by a rising column of warm moist air. Higher pressure air rushes in and upward, carrying a lot of the energy stored by a warm ocean and driving higher wind speeds and lower pressures in a self-reinforcing system.

The foundation of Amazon’s growth model is a realization that forward deployed inventory on a massive scale produces unit delivery costs that are lower, shipping distances that are shorter, and customer satisfaction that is higher. The real genius behind Amazon’s model was the insight that, by turning its supply chain infrastructure into a collaborative platform, Fulfillment by Amazon (FBA) and offering its functionality to other eCommerce sellers, it could scale so big, and so quickly, that no other online retailer could match its shipping speeds, service levels, and unit costs. Greater volumes drive lower costs, which drive lower prices, thereby attracting higher volumes, another self-reinforcing system.

For retailers who choose not to work with Amazon, the challenge now is how to tap into the power of the Amazon Growth Model. It is clear no retailer themselves can compete with the Amazon post clique logistics ecosystem. What is needed is a collaboration of retailers, brands, and marketplaces who work together as one in the same way that Amazon harnesses their growth model when they created FBA. A collaboration model has been developed and is rolling out these capabilities for Holiday 2018. This model is The MonarchFx Alliance.

To understand The MonarchFx Alliance service offerings, requires understanding of three components:

Monarch: A beautiful butterfly that has gone through reinvention and a total metamorphosis from an egg, caterpillar and cocoon, to a butterfly.

Fx: Has two meanings:

-

A modern code that indicates something is new, smart, trending, and innovative.

-

Solving the equation for “x”.

Alliance: A coming together of companies by combining certain assets, resources, and expertise to provide a new and fundamentally improved offering.

The services of The MonarchFx Alliance are to provide for the movement of inventory from the seller to the MonarchFx Fulfillment Centers (FC), the picking and packing of orders, and the delivery of what is picked/packed to the person/organization that placed the order. The providing of these services is dependent upon two factors what is ordered and where the product is to be delivered. The services identified as priorities at this point are:

-

By What Is Ordered:

-

MonarchFa – Apparel and Footwear

-

MonarchFb – Big and Bulky

-

MonarchFf – Furniture

-

MonarchFg – General Merchandise

-

MonarchFi – Industrial Distribution

-

Monarch Fz – ZZZ as in Cold (refrigerated and frozen)

-

-

By Where The Product Is To Be Delivered:

-

MonarchFa, MonarchFb, MonarchFf, MonarchFg, MonarchFz, B2C customers in the US

-

MonarchFi -B2B customers in the US

-

MonarchFc -inbound or outbound B2C cross border

-

MonarchFs – deliver to stores

-

MonarchFw – delivered to wholesale customers

-

The value proposition of The MonarchFx Alliance is:

-

The economies of scale resulting from multi-tenant, multi-channel integrated fulfillment operations.

-

The justification of an automated material handling system in localized facilities, due to the volume in each facility.

-

The reduction in final delivery distance due to multiple local fulfillment operations.

-

The economies of scale resulting from combining the deliveries of multiple sellers.

-

The leveraging of world class technology to optimize inventory allocation, order management, and operating performance.

-

The network effect of increasing the benefits of MonarchFx as more sellers join.

-

The promise that MonarchFx will focus completely on logistics and will never compete with any seller nor share or misuse any sellers’ customer or product information.

The MonarchFx Alliance is the only post clique logistics ecosystem that will work in conjunction with a company’s already in place post clique logistics network to offer the speed of delivery of Amazon, at an operating and capital cost significantly less than the cost of doing their own post clique logistics. For additional information on the MonarchFx Alliance visit our website.

5.0 IT IS NOT ABOUT BRICKS VS. CLIQUES, IT IS ABOUT BRICKS AND CLIQUES

5.1 FOOD FIGHT

A few interesting dates for some retail breakthroughs:

-

October, 2012: The release of “The Amazon Effect” video.

-

August, 2013: The release of “Amazon and Wal-Mart Facing The Titans“

-

November, 2015: “The Titans: Alibaba, Amazon and Wal-Mart“

The first video established the term “The Amazon Effect” today called Amazonification of commerce, the growth of eCommerce across all retail markets. The second video established that the US “Titans” of retail are Amazon and Wal-Mart. The third video established that globally the “Titans” are Alibaba, Amazon, and Wal-Mart. This provides an interesting backdrop to headlines of June, 2017 where “The Amazon Effect” has now advanced to the point where you read headlines such as:

-

“Clash Of The Retail Titans: Amazon Goes Head To Head With Wal-Mart”

-

“Amazon vs. Wal-Mart: Which One Will Prevail”

-

“Wal-Mart In The Crosshairs Of Amazon’s Takeover Of Whole Foods”

-

“Amazon Is Buying Whole Foods In A Quest To Beat Wal-Mart With Luxury”

The fight is really not about food, but rather the battlefield for the fight is food. The fight is the epic clash between traditional-physical retail (Brick &Mortar) and online retail (the clique of the computer key). In the boxing announcer deep voice:

“Are you ready to rumble? Welcome to the clash of the “Titans”! After years of buildup to this night we are pleased to bring you in the huge food arena, the ultimate heavyweight battle of the US retail “Titans”. In the blue trunks with orange trim representing the Bricks is the retail King of America, Wal-Mart and in the black trunks with orange trim representing Cliques is the online behemoth, Amazon!!!!”

I love the build up here to “The Epic Clash” but in reality the food fight is:

-

Not really about food: Wal-Mart is clearly the dominant player in food and will be for many years.

-

Not really a fight: It is more of an evolution of how the “bricks world” engages and embraces Cliques and how the “Cliques World” engages and embraces bricks. (Recall in 2012 in “The Amazon Effect” I ended the video with a picture of what is today the Amazon bookstore).

-

Not really a battle over customers and market share. Close to 80% of Whole Food’s customers are already Amazon Prime members, only 9% of the US households who shopped at Whole Foods in April, 2017 also shopped at Wal-Mart. In fact, Wal-Mart customers have an average annual income of $45,000 whereas Whole Food attracts households averaging $100,000 per year. However, it is interesting to note that in June, 2017, Amazon took direct aim at the Wal-Mart customer base by discounting its Prime membership program for shoppers on government assistance, a core Wal-Mart shopper.

Therefore, the point is it is not about Bricks vs. Cliques, but rather Bricks AND Cliques. What makes this so fascinating is that Amazon has decided to play this out in an arena where they have tried many things before but have not done well, where Wal-Mart is clearly the dominant player. This is not an editorial comment, it is a fact, Wal-Mart has a dominant 26.2% market share in grocery and Whole Foods and Amazon combined have less than 3% market share. If the boxing ring announcer had included the weight of the fighters to enter the ring he would have said Wal-Mart weighing in at 262 pound vs. Amazon at just less than 30 pounds. You would say, “That’s not a fair fight,” and you would be right. Do not be mistaken, this fight is not really about food, but rather about the ultimate evolution of how retail will evolve with Bricks AND Cliques. Yes, this was a very bold move by Jeff Bezos (Wal-Mart does get 56% of their US sales from grocery). We have come to expect nothing less from Bezos. For one last time the “fight analogy” do not forget about Rocky Balboa vs. Apollo Creed and also of note David vs. Goliath.

An interesting question one could ask is why Bezos would pick grocery for this roll out of Bricks AND Cliques. Consider the following thoughts:

-

As was said in Section 2.0: grocery is broken.

-

As was said in Section 4.0: eCommerce delivery for grocery is very complex and very difficult.

-

As was said in Section 3.0: Jeff Bezos has hustle and grit.

-

Not yet been said, grocery is a highly emotional shopping experience for many. There is a dichotomy of the connectivity to grocery shopping for the shopper. On the one hand grocery shopping is gathering the stuff that is needed to keep the household going. No emotional connection here. This is clearly the case for Pantry Restock. On the other hand is the role of the grocery shopper providing for the health and pleasure of themselves and loved ones? An interesting lesson here played out for Campbell Soup in China. China families have traditionally eaten a lot of soup. Several years ago Campbell Soup studied the market and created unique soup products that were healthy, convenient, and economical, their soup was a failure. The thing they missed was “It was not about the soup”! It was about the dedication of the person responsible for the cooking and the health and happiness of the family. The making of the broth, the selecting and preparing the vegetables, and the stirring and simmering of the soup to serve it at the peak of it healthiness and dining consumption was a very emotional undertaking. The Chinese cook was furious that some company was trying to replace their role of cooking the family’s meal by opening a can and placing it on the stove. In many ways today the thumping of the fruit, the selection of the lettuce, tomatoes, meat, and getting just the right bottle of wine is the experiential joy today of caring for oneself and one’s family, while Fresh and Unique Pantry will continue to be bought mostly in stores. In addition for both the person gathering food and the mindset of caring for their loved ones grocery spending is a major expenditure for most families, so economics come into play as well.

-

Lastly, the real food fight is not Bricks vs. Cliques, but rather a fight about the price and convenience of Pantry Restock. The tradeoff in the minds of the one responsible for providing meals, between the emotional joy of providing healthy enjoyable meals and price/convenience. For a single person living in New York City the thought of going to a grocery store is unthinkable. To a care giver living in a suburban home with two school age children, the thought of having some stranger pick out their fruit and meat is equally absurd.

Some in grocery do not understand. They see the blending of Bricks AND Cliques as a technology opportunity. They want to “bring technology to life in the store” they want to make store shopping more like online shopping. We read about deploying cameras and infrared sensors to monitor foot traffic, using data algorithms to do real time cashier scheduling, mobile apps that analyze shopping habits and produce relevant digital coupons, sensor-laden interactive shelves that detect shoppers in the aisles via the phone to offer deals and suggest products, creating customer “favorite lists” apps, cashier-less stores, digital shelf edges, etc. The fact is customers do not want to handle Pantry Restock. They are happy to drive up to curbside pickup for Pantry Restock to have the products placed in the car or to have it delivered to home. The choice in where and how to shop is about convenience and price, but for the most part, customers want to go to a grocery store that is efficient, clean, and convenient to do their grocery shopping for Fresh and Unique Pantry. Customers want to enjoy the experience and fun of food retail and to avoid the dull routine of shopping. The use of technology in the store that helps the store operate better is great, in the process of making the store more efficient, let’s be sure we do not use technology to interrupt the discovery, exciting, and fun part of Brick & Mortar engagement. This is the coming together of Bricks AND Cliques, not a text message offering a new cereal when one happens down the cereal aisle or while traveling from the meat department to checkout.

5.2 RETAIL TRUTH

There is a big difference between predicting the death of Brick & Mortar and predicting something new going to happen with Bricks AND Cliques. It is clear that Brick & Mortar have had many bankruptcies and many store closings, this is the result of many factors and none of those factors is the dying of Brick & Mortar. In fact, the only thing I see dying are the analysts that have been predicting the death of Brick & Mortar. The reality is the bankruptcies and store closings have more to do with an overbuilt retail landscape, consumers buying less “stuff”, and instead spending their disposal income on more experiential purchases. In fact, of the top ten US retailers, all except Amazon, are primarily Brick & Mortar and all top ten except for Target (who is recovering from a spell of weak leadership), grew in 2017. In addition, for many retailers their clique growth is greater than their brick growth. It is clear the profits flow from the brick side and not the clique. Indeed, retailers’ Brick & Mortar business is subsidizing their clique business. So, it is clear, as I said in a blog on June 2, 2017 playing off of the famous quote by Mark Twain, “The Reports of the Death of Brick & Mortar are Greatly Exaggerated”.

An interesting side note that seems to be forgotten, if it were not for Amazon and eBay, retail would be very different today. Have we forgotten the dot-com bubble? From year 2000 to 2002 all Cliques disappeared, except for Amazon and eBay. If one wished to discuss the death of Bricks or Cliques the discussion should really be how Cliques almost died 15 years ago. Brick & Mortar has not died and is not dying. However, what began with Wal-Mart buying Jet.com in August, 2016 just got put on steroids with Amazon buying Whole Foods. What we have with these two acquisitions is the beginning of a new era for retail. This new era is about Bricks AND Cliques and this new era is not a surprise. Look at what has been said by Amazon, Wal-Mart, Alibaba, and Target (not the weak management of Target, but the new, strong management of Target):

-

Jeff Bezos has said consistently for more than 15 years, “We would love to open Amazon retail stores, but we want to do something that is uniquely Amazon, but we haven’t found the idea yet.” Jeff is now talking about “Retail Innovation”.

-

Marc Lore the founder of Quidsi (which he sold to Amazon) and Jet.com (which he sold to Wal-Mart) and now the President and CEO of Wal-Mart eCommerce US said last August at the announcement of Wal-Mart buying Jet, “We started Jet with the vision of creating a new shopping experience. Today, I couldn’t be more excited that we will be joining with Wal- Mart to help fuel the realization of that vision.”

-

Jack Ma said last October in a letter to shareholders, “Pure eCommerce will be reduced to a traditional business and replaced by the concept of New Retail.”

-

Brian Cornell the new CEO of Target in February, 2017 said, “Retail is in the midst of a Seismic Shift and this shift in channel preference is real and only gaining momentum.” “How do we get just the right amount of product to exactly the right place at exactly the right time? The work underway is game-changing for Target.” This game-changing Target approach has to do with Demand-Driven Replenishment and is a core element of the future of Bricks AND Cliques.

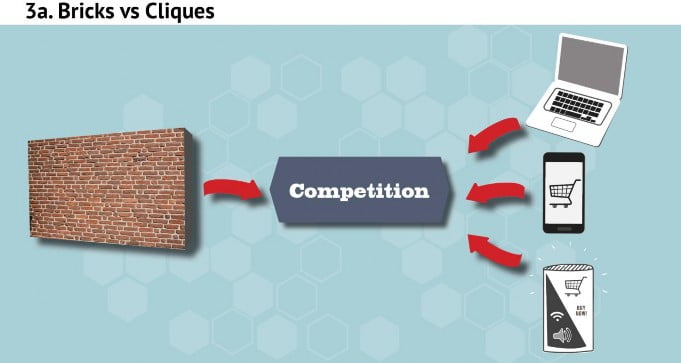

What is this “Retail Innovation”, this “New Shopping Experience”, this “New Retail”, and these “Game-Changing Shifts”? In three words, Bricks AND Cliques. To grasp this look at the progression of Bricks AND Cliques presented in Figure 3. In Figure 3a we see the traditional picture of the competition Bricks vs. Cliques as seen from the mid-1990’s until 2016.

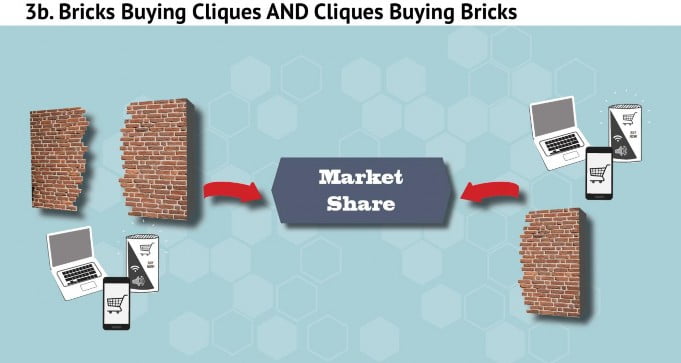

Who would win? For most of the time from the mid-1990’s to 2014 the majority opinion was that the Cliques were never going to be profitable, therefore the Bricks would win. Beginning in 2014 when the message of “Retail at a Crossroads” began to resonate, retail bankruptcies, and store closings accelerated, Amazon turned profitable, and many began posturing that Bricks were dying or dead. What began happening at about this same time was, as seen in Figure 3b, Bricks started buying Cliques and Cliques started buying Bricks.

This plus the expansion of Bricks into Cliques and Cliques into Bricks begets the need for Bricks AND Cliques to work together. The term “omnichannel” was invented to represent a retailer’s pursuit of having their channels working together, attempting to offer a seamless journey across multiple channels by supporting buy online/pick up at store, buy online/return to store, order in- store/deliver to home, etc. The Bricks buying Cliques and vise versa laid the foundation for what Alibaba, Wal-Mart, and Amazon did next. Starting in 2015, Alibaba began buying stores at a serious pace. Buying the huge supermarket chain Sanjiang, the huge department store Intime, the huge Brick and Mortar electronics chain Suning, and in May, 2017 buying 18% of Lianhua Supermarket. Then in August, 2016 Wal-Mart bought Jet.com followed in January-June, 2017 with four apparel companies Shoebuy.com, MooseJaw, Modcloth, and BONOBOS. Amazon was quiet on US acquisitions until they unleashed the big one last month of acquiring Whole Foods market. Interestingly, Amazon is buying Bricks in Wal-Mart’s strongest category, grocery, and Wal-Mart is buying Cliques in Amazon’s strongest category, apparel. This evolution then has beget the beginning of the new era of retail Bricks AND Cliques.

Figure 3c illustrates Bricks AND Cliques where the retailer offers in-store and online products where the customer decides how to explore, purchase, receive, obtain support, and interact with their retailers in a Unichannel Ecosystem.

Omnichannel are services the retailer provides for customers. Unichannel is the customer receiving the services from the retailer how they want it. You will note in Figure 3c the Unichannel customer is smiling as the ecosystem is there to serve the customer needs. The Unichannel Ecosystem is customer-centric.

Taking a different view of Bricks AND Cliques, let me just share a few thoughts with you on where this is going. The best way to address this is by understanding the top three US “New Retail” players (Amazon, Wal-Mart, and Target) and the number one Global “New Retailer”, Alibaba, is to understand:

-

Their leadership.

-

Their strengths and weaknesses.

A few thoughts on each:

-

An interesting phenomenon has occurred with how Amazon, Wal-Mart, Target, and Alibaba are evolving. In all four circumstances the firms are moving towards a Unichannel Ecosystem of Bricks AND Cliques while being lead by a Bricks leader and a Cliques leader as shown in Table 1.

-

I find it interesting how the top four “New Retail” players are responding to “New Retail”. Table 2 highlights a few of the relevant “New Retail” strengths and weaknesses.

6.0 RETAIL AGGREGATION PRECLUDES RETAILERS FROM BEING SUCCESSFUL

6.1 FOOD FIGHT

We need to begin this truth with an understanding of the concept and the danger of the concept of “Aggregation”. Aggregation is defined as:

-

A cluster of things that have been brought together.

-

Taking all units as a whole.

Aggregation is useful in that it allows us to categorize things in a way that we can understand differences between categories. It is useful to make the observations such as:

-

Home delivery of Pantry is less expensive than Fresh.

-

Margins are higher in apparel than food.

At the same time creating clusters of things that have inherent differences can result in observations that are not true. For example, with the two examples I gave:

-

Home delivery of Pantry to a farmers house in rural Kansas costs more than a Fresh delivery in New York City.

-

Margins are higher for Fresh store made sushi than for home delivery of men’s underwear.

The point is that using aggregation has value in some circumstances, but in others can result in conclusions that are wrong with others. Thus, aggregation often precludes retailers from being successful.

To dig deeper into food retail aggregation requires an in-depth understanding of the following aggregation topics:

-

Product: There are significant differences between Fresh, Pantry Restock, and Unique Pantry. Even these categories are weak. For example Fresh includes fruits, vegetables, meats, fish, dairy, frozen, etc. Even these categories may be weak as there is a difference between tomatoes and lettuce, between bananas, blueberries, etc.

-

Location: Location aggregation is important both from the location of the store and the location of the customer. Categories include big cities where people do not own cars like NYC (the largest city in the US where over half of the households do not have a car), big cities where people do own cars Houston (fourth largest city in the US where only 10% of the household do not have a car), middle sized cities where people do not own a car like Boston (the 22nd largest city in the US where more than 35% of the household do not have a car), middle sized cities where people do own a car like El Paso (the 20th largest city in the US where only 7% of the people do not own a car), small cites and onto rural.

-

Customer profile: Income level, age, education, shopping decisions made on price, convenience, experience, selection, etc.

-

And more.

The point is aggregating food retail or grocery as if it is a homogenous category can easily result in retailers making mistakes. This is why Brick & Mortar grocery executives have always had a real problem with Clique food retailers. In fact, an interesting view from FreshDirect is that they are grocery executives who do eCommerce, but Amazon executives are eCommerce executives who do food retail. This separation of Brick & Mortar grocery executives and Clique food retailers has now been brought back together as we are moving to Brick AND Clique food retailers. This intimate knowledge of grocery will prevent the Brick AND Clique food retailers from making aggregation mistakes.

6.2 RETAIL TRUTH

The greatest risk with aggregation occurs when the breath of the aggregation is great. When people use figures such as 10% of all retail is online and one third of all online purchases are returned, lumping all of retail into one category, the only thing we really know is we have bad information. For example we know only 2% of all grocery ordering is online and 60% of all office supplies are bought online. Across all categories the 10% may be accurate, the general statement 10% of all retail is online has little value. In a similar way, when someone asks an aggregate question that suggest retail is a category we need to be aware the answer will have little value. For example what is the “right” answer to these questions?

-

What is the best way to ship a retail eCommerce order?

-

What is best way to handle returns?

-

What is the best process to fulfill (pick &pack) eCommerce orders?

The right answer to each of these questions is, “It depends.” You ask, “Why?” It depends on the same factors described in section 6.1 what products, what moves, and the customer’s profile. To illustrate let’s consider the question number three on fulfillment. The more we aggregate products (the more general the response) the less efficient and effective the solution. For this reason when we discussed MonarchFx in Section 4.2 you note we highlighted the difference between MonarchFa for Apparel and Footwear, MonarchFb for Big and Bulky, MonarchFf for Furniture, MonarchFg for General Merchandise, etc. because the best way to fulfill orders in each of these categories is different. For example when designing the solution for MonarchFa we found ourselves traveling around the world, forming a new company, Tompkins Robotics, and obtaining US patents. You ask, was this focus of Apparel and Footwear really worth the effort? Fair question, you tell me. The Tompkins Robotics MonarchFa solution when compared to a more general pick module, put wall, and tilt tray conveyor has savings such as these:

-

Lead time reduced by 50%.

-

50% – 60% of the investment vs. traditional unit sorter.

-

40% – 50% faster return on investment.

-

55% – 65% of the floor space vs. traditional unit sorter.

7.0 UNIQUE IS EXCITING AND MARVELOUS, COMMON IS DULL AND UNPLEASANT

7.1 FOOD FIGHT

Eating is an important part of life. Not just eating for the sake of being hungry but also eating for pleasure. The phrase came to me as I was writing this “The Celebration of a Good meal”. Which then inspired me to do a search for interesting quotes on food, here are a few of my favorites:

-

“One cannot think well, love well, and sleep well, if one has not dined well.”

-

“I cook with wine; sometimes I even add it to the food.”

-

“The preparation of good food is merely another expression of art, one of the joys of civilized living.”

-

“I think preparing food and feeding people brings nourishment not only to our bodies but to our spirits. Feeding people is a way of loving them, in the same way that feeding ourselves is a way of honoring our own createdness and fragility.”

Whole Foods understands these quotes. Jeff Bezos recently said, “Whole Foods Market has been satisfying, delighting, and nourishing customers for nearly four decades.” I believe he understands these quotes. I would imagine Marc Lore, Doug McMillon, Arthur Valdez, and Brian Cornell understand these quotes too. However, I am not sure Amazon, Wal-Mart, or Target fully understands these quotes. I went to Whole Foods last weekend with my wife. I have not been grocery shopping with my wife in many years. Either she goes or I go. Last weekend we went together and had a ball. It was not shopping, it was an outing. It was better than a movie and the floor was not sticky.

Whole Foods is exciting and marvelous. Was it the cheese shop, the olives, the bakery, the concern for my heath, the focus on nutrition? Or was it a combination of the exploration, the learning, and the experience? For some it may be the over 5,000 private label “365 Everyday Value” products, for some the prepared foods or the over 250 places to eat. What attracted Amazon, was it the new “Whole Foods Market 365” concept or the potential for meal-kits (think Blue Apron)? “Whole Foods Market 365” only has a handful of stores open, currently over a dozen under development and appears to be inspired by the success of Trader Joe’s and Sprouts. Going to a traditional grocery store, sure you see the fruit and vegetables all stacked up, shelves full of private label and standard brands, but to me dull and uninteresting. Sure clean, organized and good customer service, but otherwise dull and not an experience.

Why not just order online and have it delivered? Or maybe soon I can go to Whole Foods, have them place the dull and uninteresting in my trunk, after I have an exciting and marvelous time in their store. Maybe even pick up my Amazon order from a locker or tower there, invite the spouse for a slice of pizza, or that oldest daughter/granddaughter on a “date night”. Exciting and marvelous, and I believe as a part of Amazon, as a part of New Retail, as a part of Bricks AND Cliques it is going to be even more exciting and more marvelous going forward.

7.2 RETAIL TRUTH

I believe the exciting and marvelous as opposed to the dull and unpleasant are clear from the discussion in 7.1 food truth. There are ways beyond the grocery store that can be exciting and marvelous. How about the thrill of the hunt at a TJ Maxx, Ocean State Jobbers, Ollies, Five Below, or a dollar store.

Or how about the second star of the Macy’s North Star Strategy, “It Must Be Macy’s: Products and experiences that can only be found at Macy’s.” Jeff Gennette, the company’s new CEO, in an exciting attempt to revive the fortunes of Macy’s is talking about edited, elevated, and exclusive assortments. The goal is to increase today’s 29% share of sales on exclusives to 40% by 2020. An exciting direction, hopefully Gennette is also able to achieve Bricks AND Cliques.

Interestingly, the call for Macy’s exclusive assortment is the awesome job Amazon is doing in apparel with 14 private label apparel brands that are exciting, but not yet marvelous due to weak assortment planning. Not to be left out is the strong push by Wal-Mart/Jet with private label through acquisition, Target and J.C. Penney revitalizing and expanding their private label outreaches. Stores full of common stuff or online offerings of common stuff are dull and uninteresting. They are in a race to lower and lower prices. Stores and online offerings full of unique items and unique experiences are vibrant, exciting, fun, and marvelous.

8.0 DATA, INFORMATION, AND INSIGHT IS PRECIOUS

8.1 FOOD FIGHT

Amazon had a hole in their bucket, or maybe for this section, a better way to say this is a hole in their shopping cart. Amazon has lots of information on us, our likes, dislikes, interests, and how we live. The hole is the lack of information about how we shop in-store. A major next step to filling this hole is Whole Foods. As Amazon fills in this hole for themselves they too will be able to more fully understand the dynamics of private label and CPG brands. They will, just as they have built for apparel and footwear, have rich data, deep information, and valuable insights into the needs and wants of their customers. To gain insights to this statement consider the comment by Nilam Ganenthiran, Chief Business Officer at Instacart, in an interview in RetailDrive last March:

“One of the benefits Instacart has is our breath of scale. Its 185 grocers, 34 markets and we’ve been doing these four-and-a-half years, so we’ve been able to bring retailers and CPG’s some deep insight into what assortments resonate with the eCommerce customer, what is different about the way they shop on-line? What are their frequency and basket patterns?”

And then another question to Ganenthiran, “What can Brick & Mortar stores do to keep people coming back to stores?” he answers:

“The best-in-class Brick & Mortar operators will do two things. They are going to view technology not as a threat, but as an enabler. And two, they are going to think about what pain points they can take away from a shopper’s day, and that involves taking seconds and minutes out of the shopping experience so there’s truly no friction when you go to a store, and any barrier between a consumer converting and buying gets removed.”

As I said in the last paragraph of Section 5.1:

“The use of technology in the store that helps the store operate better is great, in the process of making the store more efficient, let’s be sure we do not use technology to interrupt the discovery, exciting and fun part of Brick & Mortar engagement. This is the coming together of Bricks AND Cliques, not a text message offering a new cereal when one happens down the cereal aisle or while traveling from the meat department to checkout.”

A question; who do you think is best equipped to develop rich data, deep information, and valuable insights, Instacart or Amazon? I would have answered that question last March, Instacart. Now with the acquisition of Whole Foods by Amazon my answer is, Amazon. In fact, I believe a key justification of why Amazon bought Whole Foods is the process of filling the hole in the Amazon shopping cart by beginning to include Brick & Mortar data into their analytical capabilities in the pursuit of rich data, deep information, and valuable insights first in food retail and over time in all of Brick & Mortar, to go along with their already best-in-class eCommerce analytics to be the leader in Bricks AND Cliques, creating valuable insights to improve their Bricks AND Cliques business.

8.2 RETAIL TRUTH

As Amazon fills the Brick & Mortar hole in their shopping cart by making Whole Foods their pilot for developing more robust and sophisticated big data marketing strategies for Bricks AND Cliques, at first all food retailers will be under pressure to reciprocate, but as this plays out it will go beyond food and put all retailers under pressure. Although the food retailers have all been ahead of Amazon with in-store analytics and have been making significant investments in Brick & Mortar digital technology, all of a sudden they are behind as the rich data, deep information, and valuable insights needed now are not about Brick & Mortar, rather about Bricks AND Cliques. There is not a lot to say at this point about rich data, deep information, and valuable insights for Bricks AND Cliques. We do know Amazon already has a strategy, and we better establish one soon.

9.0 DO NOT BE AFRAID TO KILL SACRED COWS

There are many things that need to be changed, transformed, and reinvented, along with many sacred cows to be converted into steak, for us to all do well with this new era of retail. In fact, the evolution to the eight truths presented in this paper will result in many Brick & Mortar and online retailers failing. Many sacred cows will need to be sacrificed. In my view, the most difficult sacred

cow that needs to be eliminated is the Case Supply Chain. In Section 5.2 when we listed the strengths and weaknesses of the top four retail US players:

-

Three of the top four (Alibaba, Amazon and Wal-Mart) were weak in Demand-Driven Replenishment.

-

Two of the top four (Target and Wal-Mart) were weak in Each Picking.

Eliminating the Case Supply Chain sacred cow resolves both the Demand-Driven Replenishment and the Each Picking requirement to be a New Retailer.

In the material handling field there is a principle called the Unit Load Principle. This principle states, Unit Loads shall be appropriately sized and configured in a way which achieves the material flow and inventory objectives at each stage in the supply chain. The Unit Loads used most frequently in a retail supply chain are the container, pallet, Case, and the Each. A container of product is best to move across long distances where a large volume of product is moved. The container remains the Unit Load as long a practical. Once the container reaches its destination via ship, train, and/or truck it is unloaded and from that point the pallet is the Unit Load. The pallet Unit Load is moved by lift trucks, stored in bulk or on racks and moved through Distribution Centers (DC) for as long as practical. When it is de-palletized the Case becomes the Unit Load. Traditionally the Case was the Unit Load until the Case arrived at a store and a person took the Eaches out of the Case and placed them on a retail shelf awaiting a customer to buy the Each. This worked well for 50 years and then two major shifts took place:

-

Marketing and product development went wild and started inventing many versions, sizes, and packages of product. To hold a Case for these products required larger stores and a major increase in the dollars of inventory in the stores.

-

eCommerce began selling Direct to Consumer (DTC), obviously the consumer did not want a Case of a product, and then a shift took place in the supply chain. The DC role was no longer just replenishing stores, there was a need for a FC that received Cases in from the DC and sent Eaches DTC.

All eCommerce retailers had to establish FC to handle DTC. Sometimes these FC were in the DC, sometimes separate from the DC, and sometimes 3PL were used for FC.

Then the marketing and product development continued to go wild. When I was young we had one package size of one type of Oreo cookies. This has exploded and today there are hundreds of different types/packages of Oreos. What should a retailer do? Retailers decided to sell shelf space to the manufacturer. If Nabisco spent enough money on shelf allowances for Oreos in a supercenter they could have 50 feet of shelving, four feet high, full of Oreos. The result is a lot of inventory in the store that is slow moving and not producing the margin per square foot of store space the store desires. Since we are already doing Each pick in the FC what has become viable is to use the FC to send Eaches to the store, based upon what the store has sold since last replenished. The signal that requests this replenishment is called a Demand-Driven Replenishment signal. Are you keeping up?

The FC allows you to do Eaches, the demand signal tells you when to replenish and what we have is smaller stores (or the same sized stores with many more new items), with much less inventory, higher inventory turns, and higher in-stock performance, thus increased revenue. Of course the challenge of operating these high volume Each pick, FC is prohibitive unless systems are designed to do this (think Tompkins Robotics), or it is outsourced to organizations designed to handle this volume of Eaches (MonarchFg).

The sacred cow is the Case Supply Chain. The replacement for the obsolete Case Supply Chain for Bricks AND Cliques, is the Each Supply Chain that uses Demand-Driven Replenishment.

There are many other organizational, operational, technological, and sacred cows, in order to achieve a Unichannel Bricks AND Cliques ecosystem the Case Supply Chain must be replaced with an Each Supply Chain.

10.0 CONCLUSION

Wal-Mart began a focused drive to enhance their eCommerce performance several times, but did not seem to understand it until they bought Jet.com in August, 2016. Throughout the first six months of 2017 Wal-Mart/Jet purchased four eCommerce apparel firms. Wal-Mart clearly had entered territory that Amazon “owned”.

Amazon mounted a direct strike back at Wal-Mart. In June, 2017 they purchased a significant food retailer Whole Foods clearly territory “owned” by Wal-Mart. Are these two big players fighting about the other one’s processions? No, not really. In fact, Whole Foods and Wal-Mart grocery business are both food retailers, but they are very different. Also, Wal-Mart’s apparel acquisitions are very small in size and really do not have much impact on Amazon. If it wasn’t a fight what drove these two paths that appear to be confrontational? The answers are simple:

-

Apparel is a very fragmented industry and it is the leading online category. Wal-Mart needs to grow its online business, therefore a logical path to take.

-

Amazon has personally seen that grocery is broken, it is a huge market and it is the best opportunity for Amazon to grow their Brick & Mortar business.

Amazon is trying to become Bricks AND Cliques and has decided grocery stores are the best path to make that happen. Similarly Wal-Mart is trying to become Bricks AND Cliques and has decided eCommerce apparel is the best path to make that happen. In spite of the fun I had with Rocky Balboa vs. Apollo Creed, this is not a battle between Amazon and Wal-Mart. What is really taking place is that two great companies are watching what is happening and have realized that we are entering a new era for retail. Just like in 1988 when Sam Walton opened his first stores, today is a big deal. This is the beginning of the era of new retail, retail innovation, a new shopping experience, game-changing Demand-Driven Replenishment, an Each supply chain, exploration, and creation of Bricks AND Cliques, rich insights that come from integrating the Brick & Mortar with eCommerce data and lastly, but most importantly, putting the customer in charge of their Unichannel Bricks AND Cliques to find exciting/marvelous enjoyment, exploration, and experiences while maximizing convenience/value/selection.

What will happen next? We will continue to have obsolete retailers closing stores and going out of business. We will have lots of pain in food retail as margins continue to fall and stores/companies close. We will see Wal-Mart/Jet continue to make progress in eCommerce, we will see Amazon/Whole Foods expand and grow, and we will see Target regain their footing and prosper. We will see Amazon/Wal-Mart/Target grab hold of Bricks AND Cliques, the Each Supply Chain, and Demand-Driven Store Replenishment. Do not forget for Jeff, John, Doug, Marc, Brian, and Arthur, It is important for you to maximize your organization’s hustle and grit, while empowering your customer-centric ecosystem to make your customers happy to have you as their retailer.

11.0 CONTACT INFORMATION

James A. Tompkins, Ph.D.

Chairman and CEO

Tompkins International

www.tompkinsinc.com

Chairman and CEO

MonarchFx

www.monarchfxgo.com

Email: jtompkins@tompkinsinc.com

6870 Perry Creek Road

Raleigh, NC 27616

12.0 WORKS CITED

Abrams, Rachel, and Julie Creswell. “Amazon Deal for Whole Foods Starts a Supermarket War.” The New York Times. The New York Times, 16 June 2017. Web. 18 June 2017. https://www.nytimes.com/2017/06/16/business/whole-foods-walmart-amazon-grocery-stores.html.

Abrams, Rachel. “A Street Fight Among Grocers to Deliver Your Milk, Eggs, Bananas.” The New York Times. The New York Times, 24 June 2017. Web. 25 June 2017. https://www.nytimes.com/2017/06/24/business/a-street-fight-among-grocers-to-deliver-your-milk-eggs-bananas.html.

Activist Stocks Long/short Equity, Deep Value, Special Situations, GrowthMarketplaceCatalyst Driven Small-Caps. “Whole Foods Could Be The Next YouTube.” Seeking Alpha. N.p., 26 June 2017. Web. 28 June 2017. https://seekingalpha.com/article/4084065-whole-foods-next-youtube.

“Amazon Acquiring Whole Foods Only Validates Brick And Mortar Retail.” Seeking Alpha. N.p., 19 June 2017. Web. 21 June 2017. https://seekingalpha.com/article/4082379-amazon-acquiring-whole-foods-validates-brick-mortar-retail.

“Amazon Is Making A Big Mistake.” Seeking Alpha. N.p., 21 June 2017. Web. 23 June 2017. https://seekingalpha.com/article/4083031-amazon-making-big-mistake.

“Amazon Provides Food For Thought.” Seeking Alpha. N.p., 19 June 2017. Web. 21 June 2017. https://seekingalpha.com/article/4082386-amazon-provides-food-thought.

“Amazon: The Last Mile.” Seeking Alpha. N.p., 20 June 2017. Web. 21 June 2017. https://seekingalpha.com/article/4082552-amazon-last-mile.

“Amazon, Whole Foods, and the Dynamic Future of Retail.” Infor Retail. N.p., 21 June 2017. Web. http://inforretail.com/blog/converged-commerce/amazon-whole-foods-dynamic-future-retail/.

Berman, Laura. “This One Roadblock May Prevent Amazon and Whole Foods From Destroying Grocery Stores.” TheStreet. TheStreet, 26 June 2017. Web. 28 June 2017. https://www.thestreet.com/story/14194711/1/one-key-challenge-may-hold-back-amazon-and-whole-foods-back-from-crushing-the-grocery-store-industry.html.

Bhattarai, Abha. “What Is Lidl? 5 Things the German Grocer Is Bringing to America.” The Washington Post. WP Company, 15 June 2017. Web. 10 July 2017. https://www.washingtonpost.com/news/business/wp/2017/06/15/what-is-lidl-5-things-the-german-grocer-is-bringing-to-america/.

Bishop, Todd. “Whole Foods Delivery Partner Instacart: Amazon Just ‘declared War’ on America’s Grocery Stores.” GeekWire. N.p., 17 June 2017. Web. 30 June 2017. https://www.geekwire.com/2017/whole-foods-delivery-partner-instacart-amazon-just-declared-war-americas-grocery-stores/.

Bold, Cambria. “I Had My Groceries Delivered by Instacart, and Here’s How It Went.” Kitchn. N.p., 9 Jan. 2015. Web. 28 June 2017. http://www.thekitchn.com/i-had-my-groceries-delivered-by-instacart-and-heres-how-it-went-214795.

“Breeze In, Grab Just What You Need, Cruise on Out. You’ll Love Shopping at Whole Foods Market 365.” 365. N.p., n.d. Web. 30 June 2017. http://www.365bywholefoods.com/stores.

Cadell, Cate. “Amazon’s Grocery Push Playing Catch up with Chinese E-commerce Giants.” Reuters. Thomson Reuters, 22 June 2017. Web. 23 June 2017. http://www.reuters.com/article/us-whole-foods-m-a-amazon-china-idUSKBN19C32V.

Campbell, Todd. “3 Intriguing Ways Amazon.com Can Profit From Buying Whole Foods.” The Motley Fool. The Motley Fool, 18 June 2017. Web. 19 June 2017. https://www.fool.com/investing/2017/06/18/3-intriguing-ways-amazoncom-can-profit-from-buying.aspx.

Collins, J.G. “The Genius Of Amazon’s Whole Foods Acquisition.” Seeking Alpha. N.p., 08 July 2017. Web. 10 July 2017. https://seekingalpha.com/article/4086428-genius-amazons-whole-foods-acquisition.

Craig, Victoria. “Kroger, Walmart Have Time to Bid for Whole Foods, but Is It worth It?” Fox Business. Fox Business, 23 June 2017. Web. 28 June 2017. http://www.foxbusiness.com/markets/2017/06/23/kroger-walmart-have-time-to-bid-for-whole-foods-but-is-it-worth-it.html.

Dastin, Jeffrey. “Even With Whole Foods, Amazon Would Need Many More Warehouses to Reshape Grocery Delivery.” The New York Times. The New York Times, 23 June 2017. Web. 28 June 2017. https://www.nytimes.com/reuters/2017/06/23/business/23reuters-whole-foods-m-a-amazon-com-logistics.html.

Dastin, Jeffrey. “Even with Whole Foods, Amazon Would Need Many More Warehouses to Reshape Grocery Delivery.” Yahoo! Finance. Yahoo!, 23 June 2017. Web. 27 June 2017. https://finance.yahoo.com/news/even-whole-foods-amazon-many-234801781.html.

Detroit Bear Deep Value, Special Situations, Long-term Horizon, ValueDetroit Bear on Twitter.cls-1{fill:#024999;}. “Amazon’s Midas Touch Hits Whole Foods.” Seeking Alpha. N.p., 16 June 2017. Web. 19 June 2017. https://seekingalpha.com/article/4082099-amazons-midas-touch-hits-whole-foods.

Domm, Patti. “Amazon’s Whole Foods Deal May Accelerate the Fresh Food Takeover, Hurting General Mills.” CNBC. CNBC, 19 June 2017. Web. 21 June 2017. http://www.cnbc.com/2017/06/19/amazons-whole-foods-deal-may-accelerate-the-fresh-food-takeover-hurting-general-mills.html.

Formichelli, Linda. “Analyst Says Whole Foods Competitors Are ‘Screwed’ After Amazon Deal.” Forbes. Forbes Magazine, 18 June 2017. Web. 19 June 2017. https://www.forbes.com/sites/lindaformichelli/2017/06/18/analyst-says-whole-foods-competitors-are-screwed/.

Gallagher, Dan. “Amazon Just Got Closer to You.” Wall Street Journal 19 June 2017: n. pag. Print.

Garcia, Tonya. “Amazon ‘will Be a Top 5 Grocer in the U.S.’ with Whole Foods Acquisition.” MarketWatch. N.p., 30 June 2017. Web. 19 June 2017. http://www.marketwatch.com/story/amazon-will-be-a-top-5-grocer-in-the-us-with-whole-foods-acquisition-2017-06-16.

Gasparro, Annie, and Heather Haddon. “How a Pioneer Lost Its Way.” Wall Street Journal. N.p., n.d. Web. 17 June 2017.

Gasparro, Annie, and Laura Stevens. “Amazon’s Grocery Ambitions Spell Trouble for Big Food Brands.” The Wall Street Journal. Dow Jones & Company, 26 June 2017. Web. 26 June 2017. https://www.wsj.com/articles/amazons-grocery-ambitions-spell-trouble-for-big-food-brands-1498469402.

Gasparro, Annie, and Laura Stevens. “Food Brands Face Squeeze From Amazon.” Wall Street Journal 27 June 2017: n. pag. Print.

Gasparro, Annie. “Kroger Shares Slide, as Grocer Is Battered by Price Fight.” The Wall Street Journal. Dow Jones & Company, 15 June 2017. Web. 10 June 2017. https://www.wsj.com/articles/kroger-shares-slide-as-grocer-is-battered-by-price-fight-1497531764.

Grant, Charley. “It’s 30% Off In All Aisles At Kroger.” Wall Street Journal 17 June 2017: n. pag. Print.

Haddon, Heather, and Julie Jargon. “Amazon’s Whole Foods Deal Adds Pressure on Grocery Services to Deliver.” The Wall Street Journal. Dow Jones & Company, 29 June 2017. Web. 30 June 2017. https://www.wsj.com/articles/amazons-whole-foods-deal-adds-pressure-on-grocery-services-to-deliver-1498728601.

Haddon, Heather. “Pressure on U.S. Grocers Rise.” Wall Street Journal 12 June 2017: n. pag. Print.

Hardon, Heather, and Julie Jargon. “Fresh Pressure on Grocery Delivery — WSJ.” Wall Street Journal 30 June 2017: n. pag. Wall Street Journal. Web.

Helmore, Edward. “Clash of the Retail Titans: Amazon Goes Head to Head with Walmart.” The Guardian. Guardian News and Media, 24 June 2017. Web. 28 June 2017. https://www.theguardian.com/business/2017/jun/24/amazon-whole-foods-groceries-walmart.

Hirsch, Lauren, and Jeffrey Dastin. “Amazon to Buy Whole Foods for $13.7 Billion, Wielding Online Might in Brick-and-mortar World.” Reuters. Thomson Reuters, 17 June 2017. Web. 19 June 2017. http://www.reuters.com/article/us-whole-foods-m-a-amazon-idUSKBN1971QJ.

“How Amazon and Walmart’s Rivalry Will Reinvent Retail.” Knowledge@Wharton. N.p., 27 June 2017. Web. 28 June 2017. http://knowledge.wharton.upenn.edu/article/amazon-vs-walmart-one-will-prevail/.

“How Does Instacart Make Money?” VatorNews. N.p., 02 Aug. 2016. Web. 28 June 2017. http://www.vator.tv/news/2016-08-02-how-does-instacart-make-money.

Huet, Ellen, and Olivia Zaleski. “Instacart Tries to Hang On to Whole Foods as Amazon Swoops In.” Bloomberg.com. Bloomberg, 16 June 2017. Web. 30 June 2017. https://www.bloomberg.com/news/articles/2017-06-16/instacart-tries-to-hang-on-to-whole-foods-as-amazon-swoops-in.

Hurtibise, Ron. “Whole Foods Bringing Value-oriented ‘365’ Chain to Delray Beach.” Sun-Sentinel.com. N.p., 07 July 2017. Web.

Ignatius, Adi. “An Inside Look at the Ups and Downs of Walmart’s Journey.” Harvard Business Review. N.p., 21 Feb. 2017. Web.

“Instacart.” Wikipedia. Wikimedia Foundation, n.d. Web. 28 June 2017. https://en.wikipedia.org/wiki/Instacart.

Jargon, Julie, and Heather Haddon. “For Amazon, Now Comes the Hard Part.” Wall Street Journal 19 June 2017: n. pag. Print.

Johnson, Eric. “Is There Room for Both Amazon and Walmart?” Recode. Recode, 07 July 2017. Web. 10 July 2017. http://www.recode.net/2017/7/7/15924064/amazon-walmart-whole-foods.

Jordan, Karen. “Whole Foods 365 To Open Three More Locations.” Bisnow. N.p., 29 June 2017. Web. 30 June 2017. https://www.bisnow.com/los-angeles/news/retail/whole-foods-76029.

Kaufman, Alexander C. “Amazon Is Buying Whole Foods In A Quest To Beat Walmart With Luxury.” Huffington Post. N.p., 16 June 2017. Web. 19 June 2017.

Kemmsies, Walter. “All Eyes on Omnichannel.” American Shipper June (2017): 31. Print.

Khan, Lina. “Amazon Bites Off Even More Monopoly Power.” The New York Times. The New York Times, 21 June 2017. Web. 21 June 2017. https://www.nytimes.com/2017/06/21/opinion/amazon-whole-foods-jeff-bezos.html.

“Kroger Could Fight Amazon for Whole Foods, Analysts Say.” Bizjournals.com. N.p., 18 June 2017. Web. 19 June 2017. https://www.bizjournals.com/cincinnati/news/2017/06/20/kroger-could-fight-amazon-for-whole-foods-analysts.html.

“Kroger Takes $7 Billion Hit as Amazon Deal Compounds Struggles.” The Spokesman Review. N.p., 19 June 2017. Web. 21 June 2017.

Lahart, Justin, and Spencer Jakab. “Amazon’s Margin Squeeze Is on Menu.” Wall Street Journal. N.p., 17 June 2017. Web. 17 June 2017.

Lien, Tracey. “How the Amazon-Whole Foods Deal Could Hurt – or Help – Instacart.” Los Angeles Times. Los Angeles Times, 20 June 2017. Web. 30 June 2017. http://www.latimes.com/business/technology/la-fi-tn-instacart-amazon-whole-foods-20170619-htmlstory.html.

Lindner, Matt. “Can Stores Give E-retailers an Edge?” Internet Retailer April (2017): 23. Web.

Loria, Keith. “Instacart’s ‘grocery Nerd’ Talks about How to Make E-commerce Work.” Retail Dive. N.p., 16 Mar. 2017. Web. http://www.retaildive.com/news/instacarts-grocery-nerd-talks-about-how-to-make-e-commerce-work/438275.

Loten, Angus. “Amazon, Whole Foods Deal to Drive Grocery Stores’ Digital Push.” The Wall Street Journal. Dow Jones & Company, 16 June 2017. Web. 21 June 2017. https://blogs.wsj.com/cio/2017/06/16/amazon-whole-foods-deal-to-drive-grocery-stores-digital-push/.

Mackintosh, James. “Blind Faith in Bezos May Sting Investors.” Wall Street Journal 23 June 2017: n. pag. Print.

Manjoo, Farhad. “In Whole Foods, Bezos Gets a Sustainably Sourced Guinea Pig.” The New York Times. The New York Times, 17 June 2017. Web. 19 June 2017. https://www.nytimes.com/2017/06/17/technology/whole-foods-amazon-jeff-bezos.html.

Michael Rogus Long/short Equity, Value, Special Situations, Foreign CompaniesPeba Tandem.cls-1{fill:#024999;}. “Target: Show Courage And Quit.” Seeking Alpha. N.p., 26 June 2017. Web. 28 June 2017. https://seekingalpha.com/article/4083822-target-show-courage-quit.

Monk, Dan. “Can Kroger Co. (KR) Survive a Giant Challenge? Hint: It Already Did.” WCPO. N.p., 25 June 2017. Web. 23 June 2017. http://www.wcpo.com/news/insider/can-kroger-survive-a-giant-challenge-hint-it-already-did.

Nash, Kim S. “At Kroger, Technology Is Changing the Grocery-Store Shopping Experience.” The Wall Street Journal. Dow Jones & Company, 20 Feb. 2017. Web. 23 Feb. 2017. https://www.wsj.com/articles/at-kroger-technology-is-changing-the-grocery-store-shopping-experience-1487646362.

Nassauer, Sarah, and Imani Moise. “Wal-Mart in the Crosshairs of Amazon’s Takeover of Whole Foods.” The Wall Street Journal. Dow Jones & Company, 16 June 2017. Web. 19 June 2017. https://www.wsj.com/articles/wal-mart-buys-online-retailer-bonobos-for-310-million-1497621286.

Nicolaou, Anna. “Subscribe to Read.” Financial Times. N.p., 17 June 2017. Web. 19 June 2017. https://www.ft.com/content/bca88eac-52f6-11e7-bfb8-997009366969?tagToFollow=.

“No Time for Grocery Shopping? Instacart Delivers.” 4-Traders.com | Stock Exchange Quotes| Company News. N.p., 21 June 2017. Web. 30 June 2017. http://www.4-traders.com/news/No-time-for-grocery-shopping-Instacart-delivers–24633528/.

Peterson, Hayley. “Whole Foods’ New Stores Are Unrecognizable.” Business Insider. Business Insider, 28 Apr. 2016. Web. 26 June 2017. http://www.businessinsider.com/inside-whole-foods-new-365-stores-2016-4.

Phillips, Erica E., and Jennifer Smith. “Amazon’s Deal for Whole Foods Seen as Ideal for Urban Pickup and Delivery Hubs.” The Wall Street Journal. Dow Jones & Company, 17 June 2017. Web. 19 June 2017. https://www.wsj.com/articles/amazons-deal-for-whole-foods-seen-as-ideal-for-urban-pickup-and-delivery-hubs-1497700800.

Raven, Benjamin. “Amazon Plans Cuts to Make Whole Foods Competitive with Walmart, Reports Say.” MLive.com. MLive.com, 19 June 2017. Web. 21 June 2017. http://www.mlive.com/news/us-world/index.ssf/2017/06/amazon_whole_foods_cuts.html.

“Retail Newsline: What Amazon’s Acquisition of Whole Foods Really Means…A Conversation with Ben Conwell and Garrick Brown.” Cushman & Wakefield Blog. N.p., 21 June 2017. Web.

Rogers, Jennifer. “Online Grocer FreshDirect Is Taking on Amazon and Wal-Mart.” Yahoo! Finance. Yahoo!, 20 Feb. 2017. Web. 10 July 2017. https://finance.yahoo.com/news/online-grocer-freshdirect-is-taking-on-amazon-and-wal-mart-145035663.html.

“A Run-down of Large Deals in Amazon.com Inc.’s History.” Fox Business. Fox Business, 16 June 2017. Web. 19 June 2017. http://www.foxbusiness.com/features/2017/06/16/run-down-large-deals-in-amazon-com-inc-s-history.html.

Smith, Tammie. “Walmart Remains No. 1 in Local Grocery Rankings; Kroger a Close Second.” Richmond Times-Dispatch. N.p., 17 June 2017. Web. 19 June 2017. http://www.richmond.com/business/local/walmart-remains-no-in-local-grocery-rankings-kroger-a-close/article_4648b39a-3c3c-5e28-bbf7-091ee43cca5c.html.

Soper, Spencer, and Alex Sherman. “Amazon Robots Poised to Revamp How Whole Foods Runs Warehouses.” Bloomberg.com. Bloomberg, 26 June 2017. Web. 28 June 2017. https://www.bloomberg.com/news/articles/2017-06-26/amazon-robots-poised-to-revamp-how-whole-foods-runs-warehouses.